What follows are two more articles re...

But first, a prefatory remark:

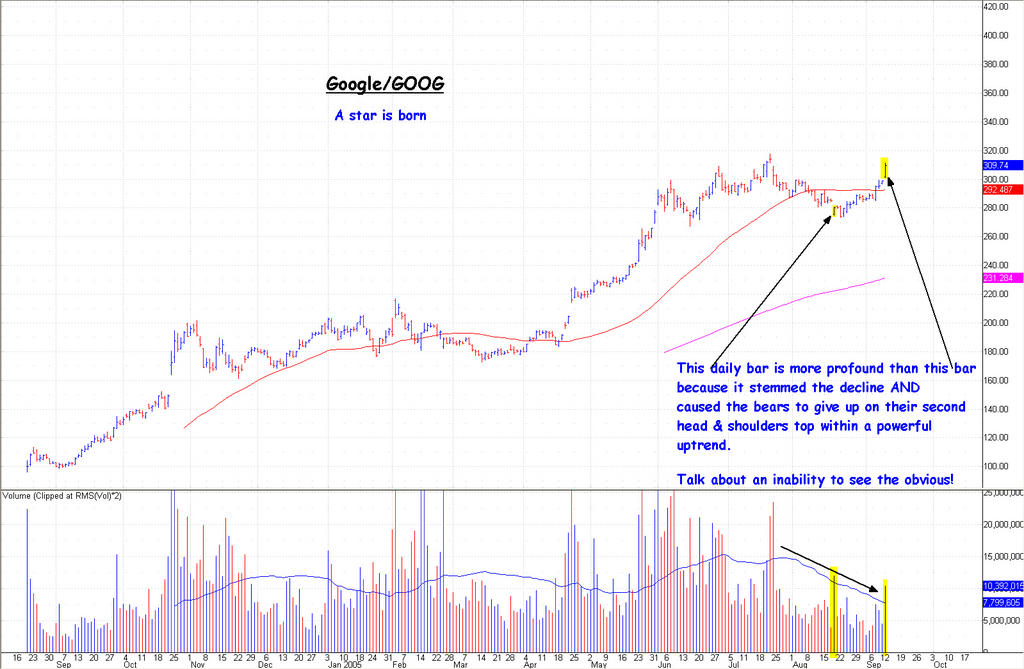

I find especially interesting the speculation re Google's purchases of dark fiber. I have previously mooted whether Google would be better served as owner or renter of this asset; now, I note the budding bottom-type chart activity in Broadwing/BWNG and especially Level 3/LVLT. It seems Wall St begins to anticipate a change in dynamics in this sector. Obviously a sudden change of heart re dark fiber occurs: to undervalued asset from over-priced albatross. The once capacious bandwidth and data networks suddenly could become bottle-necked. Especially as ever-larger files (such as videos) increasingly squirt up, down, and through the network.

As I suggested before, it is cheaper for Google, if this is their intent, to build an optical fiber network via buying the assets on Wall St for pennies on the dollar rather than building from scratch. Always playing their cards close to their (corporate) vest, the going gets interesting. But I already said that.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Link

Google builds an empire to rival Microsoft

By Elinor Mills

Google's one-of-a-kind computer network gives it a chance to surpass Microsoft to become the most dominant company in tech, according to the author of a recently published book on the search giant.

Google already has plenty of influence. It handles nearly half of the world's Web searches. It's hiring some of the biggest names in the industry, from the controversial Kai-Fu Lee of Microsoft to the legendary Vint Cerf, an early Internet pioneer. And it has become such the topic du jour in Silicon Valley that its search for a new corporate chef warrants significant local news coverage.

But what's next? Author Stephen Arnold has closely analyzed Google patents, engineering documents and technology and has concluded that Google has a grand ambition--to push the information age off the desktop and onto the Internet. Google, he argues, is aiming to be the network computer platform for delivering so-called "virtual" applications, or software that allows a user to perform a task on any device with an Internet connection.

"Google is this era's transformational computing platform and could be about to unseat Microsoft from its throne," Arnold writes in a summary of his book, "The Google Legacy: How Google's Internet Search is Transforming Application Software," published this month.

For all of its wild success, about 99 percent of Google's revenue still comes from advertising, mostly from Internet keyword searches. Certainly, it has built on the core business, adding everything from the Gmail free Web-based e-mail service to Google Earth, a satellite mapping service. And it has plenty of cash to spend on new technology--nearly $7 billion in cash, $4 billion alone from a secondary stock offering on Sept. 14.

The big question, of course, is what exactly CEO Eric Schmidt & Co. plan to do with that war chest.

In his book, which is available in electronic PDF form only, Arnold concludes that Google has created a supercomputer ready to deliver a host of applications to anyone with a Web browser.

"Google is setting itself up to be an application delivery system for any type of device," said Arnold, who has been a technology and financial analyst for 30 years. He has helped build the technology management practice at Booz Allen & Hamilton, served as a technology strategy officer at Ziff Communications, and worked on US West's electronic yellow pages and personalization tools used by @Home. "That is a different type of paradigm from Microsoft's" desktop-centric world, he said.

Arnold's research goes well beyond speculation that Google will buy Chinese portal Baidu.com, in which it already owns a small stake, or move further into the soon-to-explode voice over Internet Protocol market, beyond its voice chat-enabled Google Talk instant-messaging service.

The notion of a network computer isn't new. Sun Microsystems CEO Scott McNealy has for years been saying "the network is the computer." Oracle CEO Larry Ellison formed a company around the idea. It was called the "New Internet Computer Company," and it sold Web surfing devices before shuttering two years ago.

But unlike Sun and Oracle, Google's timing could be impeccable, Arnold argues. "Sun defined it. Ellison tried to build it. But Google owns it," he said.

The secret sauce

In short, from early on, Google founders Sergey Brin and Larry Page resourcefully figured out how to cluster lots of cheap servers and open-source software, configured to act like individual light bulbs on a Christmas tree that can be added or replaced without making the whole tree go dark, according to Arnold.

Indeed, Google representatives proudly display the company's unique rack-mounted server system to visitors to the Mountain View, Calif., campus.

"Google's architecture can scale. Using commodity hardware, Google can deploy more capacity at a lower cost and more quickly than a competitor relying on a system built with brand-name hardware," Arnold writes in his book.

Google's move into Web services--its Desktop Search and Sidebar products, for example--has prompted Microsoft to reorganize and combine MSN with its platform products group to help the software giant fight off Google's encroachment on its turf, said Frank Gillett, an analyst at Forrester Research.

Dark fiber, wireless

The reports of Google's interest in unused fiber optic, also known as "dark fiber," seems to support Arnold's theory.

"Dark fiber will enable greater dependency on what I call virtual applications," he said. "Once those high-speed connections link the dozen or so Google data centers, they will do stuff better, enable much more than telephony, media delivery."

Joe Kraus, a founder of the Excite.com portal that merged with Internet service provider @Home before filing for Chapter 11 bankruptcy in 2001, agreed that Google executives are likely thinking big, although he acknowledged he "doesn't have the slightest clue" what they are doing.

"They've been buying dark fiber for a good five years. It allows them to have such cheap communications between all their data centers," said Kraus, chief executive of online start-up JotSpot.

"A lot of people have talked about Google's core ability to host thousands of applications and being your desktop in the sky," he said. "They certainly never fail to take advantage of it when launching new products."

Google also has invested in Current Communications Group, a provider of broadband-over-power-line technology. In addition, there are rumors that Google is eyeing satellite, technology that drives its 3D Google Earth application.

"They said, back when they invested in the Internet-over-power-lines company, that part of their corporate mission is 'promoting universal access to the Internet for users,'" said Danny Sullivan, editor of Search Engine Watch. "They seem to think they need to make sure everybody can get online, and running your own network certainly makes that a lot easier."

This week, Google quietly launched Google Secure Access, a beta version of a downloadable client application that allows users to establish a secure, encrypted network connection while using a Wi-Fi wireless network. The program can be downloaded at certain Google Wi-Fi locations in the San Francisco Bay Area, Google said, without stating exactly where those locations are.

The company also has been working with San Francisco company Feeva on Wi-Fi access since earlier this year, Feeva spokesman Keith Kamisugi confirmed Tuesday. He declined to elaborate, except to say that Feeva and Google offer a free Wi-Fi hot spot at the trendy Union Square shopping area in downtown San Francisco. People who connect to the network see a Google Search splash page, Kamisugi said.

"(Google seems) to think they need to make sure everybody can get online, and running your own network certainly makes that a lot easier." --Danny Sullivan, editor, Search Engine Watch

Google spokesman Nate Tyler told Reuters that it was running a limited test of a free wireless Internet service, called Google Wi-Fi, with hot spots in a pizza parlor and a gym located near the company's headquarters.

Google also recently purchased Android, a wireless software start-up, and was looking to hire a global infrastructure strategic negotiator to ink dark fiber contracts as part of a "global backbone network."

Offering Internet access gets more potential Google users online and gives the company another way to target consumers with ads, particularly location-based advertisements for wireless users.

Google, which tends to keep long-term plans under wraps, did not return an e-mail seeking comment for this story. (Google representatives have instituted a policy of not talking with CNET News.com reporters until July 2006 in response to privacy issues raised by a previous story.)

Some people speculate the company will use the dark fiber to build a massive nationwide network that would rival those of some of the largest Internet backbone providers such as MCI and AT&T. As that theory goes, Google would use this network to shuttle traffic across the country between its data centers. Then it would use a wireless network to distribute the content locally to end users.

Voice, video

Voice over Internet communications is also a likely target, analysts said.

"If the traffic is flowing across the Internet, you have no idea how many routers the traffic has gone through, which can impact the quality of the call," said Michael Howard, an analyst at Infonetics Research. "But if the traffic travels on your own network, you can control the quality. That could be reason enough to build a network."

Video is another possibility. Google hosts people's downloaded video for free and indexes and searches it.

"It's pretty evident that they will have some play in video distribution. How that's going to come out is still a mystery," said Vamsi Sistla, director of broadband and digital home/media at ABI Research.

Like many other large companies with high bandwidth needs, Google could be building its own network simply to be saving money.

"I would imagine that Google must be paying someone a lot of money to keep its data centers running and in sync," Howard said. "So it makes perfect sense for them to build a network themselves to connect their data centers."

Gartner analyst Allen Weiner, who predicts Google will eventually develop a Google phone, said becoming an application delivery platform would be "part of (Google's) intellectual property DNA."

"If they built out a hosting platform for people to upload all kinds of content that could be searched by Google and monetized by Google, like video and podcasts...it takes money to do, and with the search capabilities as their strong suit it could be something they could do," Weiner said. "Google could say, 'We'll host it for you; you point to us.' That could be huge."

CNET News.com's Marguerite Reardon and Martin LaMonica contributed to this report.

Copyright ©1995-2005 CNET Networks, Inc. All rights reserved.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

http://www.nypost.com/business/28353.htm

September 22, 2005

GOOGLE FEELING LUCKY

By SAM GUSTIN

Google's move to lease a huge space in Chelsea is part of the technology giant's plan to build its own fiber optic network and become a bigger player in the booming Internet telephone and wireless businesses.

The company is reportedly in talks to lease a whopping 270,000 square feet in the former Port Authority Commerce Building at 111 Eighth Ave. at W. 15th Street.

The massive building is one of New York's most important so-called telecom carrier hotels — home to thousands of Web servers and other critical technology infrastructure.

"111 Eighth Avenue is the premier telecom and data facility in the United States," said Neal McGraw, the chief financial officer of NYC Connect LLC, which operates a facility in the building that allows tenants to connect their networks efficiently and at a low cost.

A spokesman for Taconic Investments, the building's owner, would not comment on the Google report.

In recent months, Google has been actively shopping for miles of "dark fiber," the unused fiber optic cable that has laid dormant since the telecom bubble burst five years ago.

Thousands of miles of dark fiber are available throughout the U.S., but the high cost of making it operational has left much of it unused. Cash-rich Google is perfectly poised to begin snapping it up.

"They are building a network," said Hunter Newby, chief strategy officer with telecom specialist firm Telx. "None of us have ever seen any type of network buildup on this scale before."

In a tantalizing hint at its plans for the future, the company has posted a job opening for a "Strategic Negotiator, Global Infrastructure," who will be charged with "identification, selection, and negotiation of dark fiber contracts both in metropolitan areas and over long distances as part of development of a global backbone network."

"If Google owned the backbone, it could provide optimal data paths for its voice and data customers," said Rob Enderle of technology consulting firm The Enderle Group. "It would give Google a sustainable advantage."

111 Eighth Ave.'s concentration of interconnected networks would allow Google to offer its new voice-over-Internet service, Google Talk, more efficiently and at lower cost because it would be able to connect directly to the networks of many of the world's leading telecom firms that are also housed there.

A Google spokesperson said the company had no announcements to make about new facilities.

The building already houses server farms for dozens of leading phone, cable and Internet companies, such as BellSouth, MCI, Qwest, and Sprint.

Allen Weiner, research director with tech consulting firm Gartner, said a fiber optic network would allow Google to create Wi-Fi networks that would allow users to make calls using Google Talk from their laptops and other mobile devices.

{kind=link}