US$ strength is relative

All comments (below) are from Scott Grannis, chief economist at Western Asset Management...

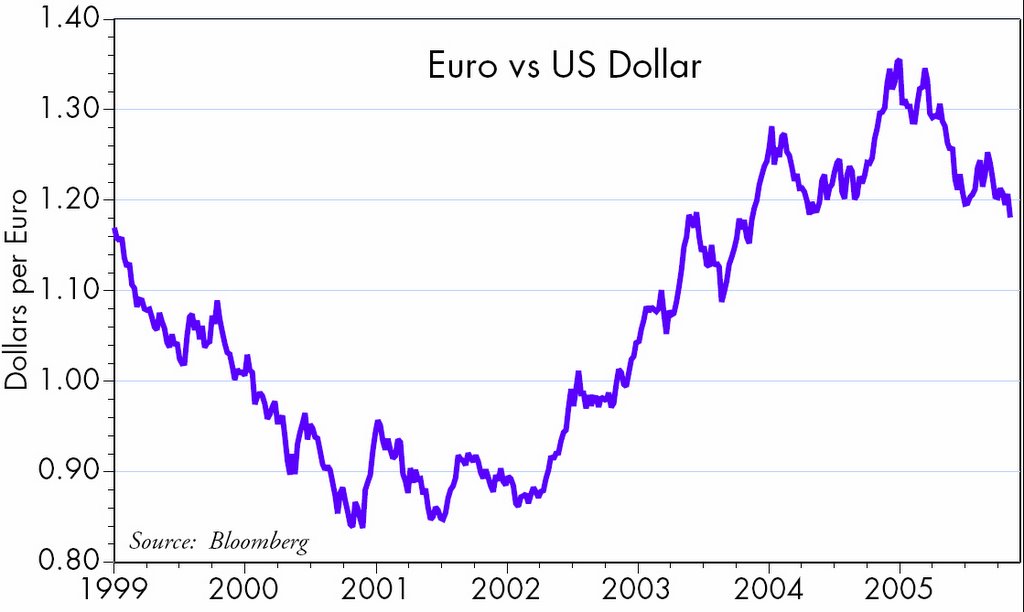

The dollar has gained almost 15% versus the euro so far this year, and it is up 13% against a broad basket of currencies. This is certainly welcome news for Americans travelling abroad, but it greatly overstates the true extent of the dollar's strength. As the second chart attached shows, the real story this year is that all currencies are declining relative to gold, and the dollar is "strong" only because it has declined by less. Year to date, gold is up 6.3% in dollars, 22.2% in euros, and 21.7% in yen. This year all currencies have lost purchasing power relative to objective standards such as gold, energy, most commodities, and real estate.

So while dollar strength versus other currencies is always better (for the U.S.) than weakness, the gains this year must be taken in the context of other, and larger losses. It is not unreasonable to think that the dollar's gain relative to other currencies owes much to the fact that the Fed has raised short-term interest rates 175 bps while most other central banks have been idle. The Fed has moved from an outright accommodative posture to a more neutral posture, and on the margin this is definitely good. But neither the Fed nor most other central banks can be said to be "tight." At least not yet.

The other implication of this year's developments is that non-dollar currencies have weakened by all objective standards. They've now "caught up" to the dollar, so in that sense inflation risk is now more evenly distributed among major countries. Since U.S. interest rates are now higher than those in every major country, with the notable exception of Australia, the dollar could enjoy further gains going forward relative to other currencies.

The dollar has gained almost 15% versus the euro so far this year, and it is up 13% against a broad basket of currencies. This is certainly welcome news for Americans travelling abroad, but it greatly overstates the true extent of the dollar's strength. As the second chart attached shows, the real story this year is that all currencies are declining relative to gold, and the dollar is "strong" only because it has declined by less. Year to date, gold is up 6.3% in dollars, 22.2% in euros, and 21.7% in yen. This year all currencies have lost purchasing power relative to objective standards such as gold, energy, most commodities, and real estate.

So while dollar strength versus other currencies is always better (for the U.S.) than weakness, the gains this year must be taken in the context of other, and larger losses. It is not unreasonable to think that the dollar's gain relative to other currencies owes much to the fact that the Fed has raised short-term interest rates 175 bps while most other central banks have been idle. The Fed has moved from an outright accommodative posture to a more neutral posture, and on the margin this is definitely good. But neither the Fed nor most other central banks can be said to be "tight." At least not yet.

The other implication of this year's developments is that non-dollar currencies have weakened by all objective standards. They've now "caught up" to the dollar, so in that sense inflation risk is now more evenly distributed among major countries. Since U.S. interest rates are now higher than those in every major country, with the notable exception of Australia, the dollar could enjoy further gains going forward relative to other currencies.

posted by David M Gordon | 12:01 PM

![]()

<< Home