Productivity and Inflation

The following comments are from Scott Grannis, Chief Economist at Western Asset Management...

The other day while riding the tube, I noticed an article in the FT that raised the issue of whether "core" measures of inflation (ex food and energy) were still relevant in these days of ever-rising energy costs. I have been questioning this as well, and have come to believe that "core" inflation that ignores years of rising energy costs is only relevant if it is also the case that other prices (non-energy prices) are falling, since that would be an excellent sign that monetary policy was not allowing higher energy costs to be passed through to the general price structure. The chart below suggests to me that monetary policy on the contrary is allowing the general price level to rise. The GDP deflator is ultimately the best long-term measure of inflation that I know of, and it is in a rising trend, albeit still a modest one.

For years I've been tracking the relationship between inflation and productivity. Most people think that strong productivity leads to low inflation, since it implies lots of competition and plentiful supplies of goods and services. I've argued instead that low inflation leads to strong productivity, since the absence of pricing power is a powerful incentive to cut costs; if you can't raise your prices the only way to make more money is to work harder and smarter. A few years ago as it became apparent that Fed policy was quite accommodative and inflation pressures were rising, I therefore expected productivity to decline. And indeed this appears to be the case. The gradual return of pricing power has dampened the incentive to be productive.

Having said that, the government announced today that productivity in the third quarter jumped to a 4.1% annual rate. But it is only up 3% in the past 12 months, and up only at a 2.6% annualized pace over the past two years. As the second chart shows, productivity has demonstrably slowed in recent years from a 4% pace to a 2.5% pace, and inflation has risen to levels not seen since the early 1990s. Last quarter's productivity surge was most likely an aberration on the high side.

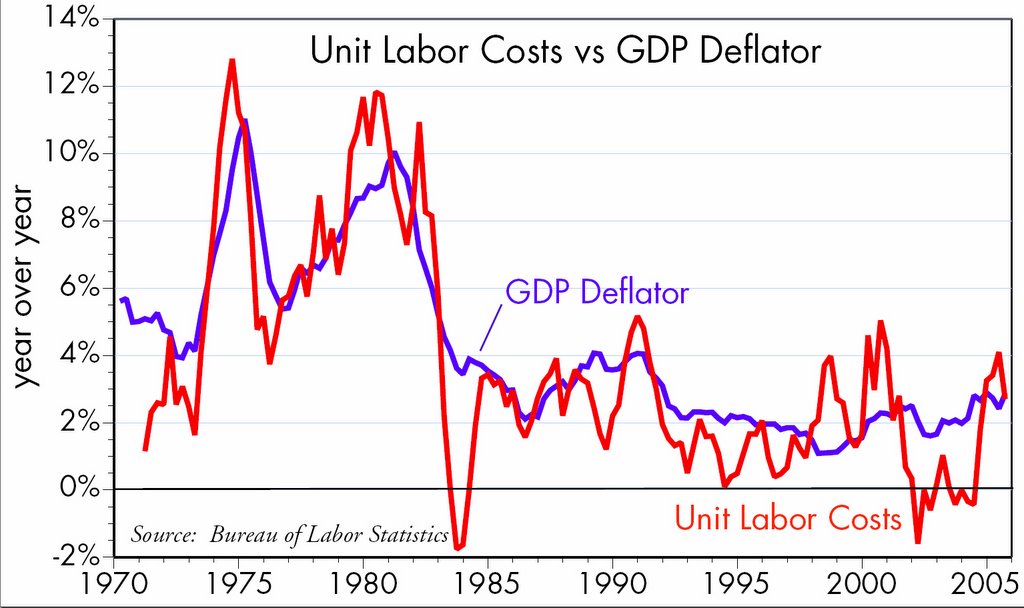

Unit labor costs fell 0.5% last quarter, in what was also probably an aberration on the low side. As the third chart shows, unit labor costs over the past year have risen by roughly the same as underlying inflation, after several years of virtually no growth at all (i.e., when labor productivity was high).

Going forward, I would expect inflation according to the GDP deflator to be 3% or a bit more, and productivity to be 2.5% or a bit less. That would imply a CPI of 3.5% or a bit more, and real GDP growth that is still in a 3-4% range.

The other day while riding the tube, I noticed an article in the FT that raised the issue of whether "core" measures of inflation (ex food and energy) were still relevant in these days of ever-rising energy costs. I have been questioning this as well, and have come to believe that "core" inflation that ignores years of rising energy costs is only relevant if it is also the case that other prices (non-energy prices) are falling, since that would be an excellent sign that monetary policy was not allowing higher energy costs to be passed through to the general price structure. The chart below suggests to me that monetary policy on the contrary is allowing the general price level to rise. The GDP deflator is ultimately the best long-term measure of inflation that I know of, and it is in a rising trend, albeit still a modest one.

For years I've been tracking the relationship between inflation and productivity. Most people think that strong productivity leads to low inflation, since it implies lots of competition and plentiful supplies of goods and services. I've argued instead that low inflation leads to strong productivity, since the absence of pricing power is a powerful incentive to cut costs; if you can't raise your prices the only way to make more money is to work harder and smarter. A few years ago as it became apparent that Fed policy was quite accommodative and inflation pressures were rising, I therefore expected productivity to decline. And indeed this appears to be the case. The gradual return of pricing power has dampened the incentive to be productive.

Having said that, the government announced today that productivity in the third quarter jumped to a 4.1% annual rate. But it is only up 3% in the past 12 months, and up only at a 2.6% annualized pace over the past two years. As the second chart shows, productivity has demonstrably slowed in recent years from a 4% pace to a 2.5% pace, and inflation has risen to levels not seen since the early 1990s. Last quarter's productivity surge was most likely an aberration on the high side.

Unit labor costs fell 0.5% last quarter, in what was also probably an aberration on the low side. As the third chart shows, unit labor costs over the past year have risen by roughly the same as underlying inflation, after several years of virtually no growth at all (i.e., when labor productivity was high).

Going forward, I would expect inflation according to the GDP deflator to be 3% or a bit more, and productivity to be 2.5% or a bit less. That would imply a CPI of 3.5% or a bit more, and real GDP growth that is still in a 3-4% range.

posted by David M Gordon | 2:33 AM

![]()

<< Home