Federal revenues surge + Weekly claims still declining, jobs market healthy

The following comments are from Scott Grannis, Chief Economist at Western Asset Management...

If I had to pick the most bullish indicator of the economy's health, this would be it. Taxes paid to the federal government in 2005 were 14% higher than in 2004. It is undeniably the case that corporate profits, personal incomes, and capital gains realizations are very strong, much stronger than anyone would have expected. Government statistics don't always pick up everything going on in the economy, but when tax revenues surge like this, you can be sure that the economy is very healthy. Even though federal revenues grew a robust 8.1% last year, the budget deficit fell from $400 billion to $320 billion, a mere 2.5% of GDP.

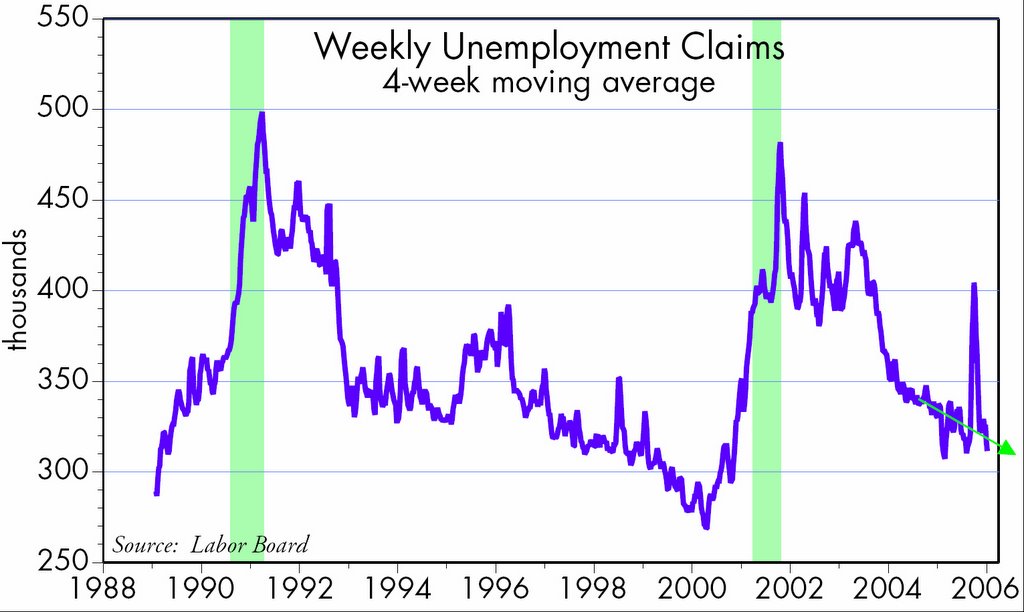

First-time unemployment claims rose last week, but the 4-week average remains in a declining trend, as the chart (below) shows.

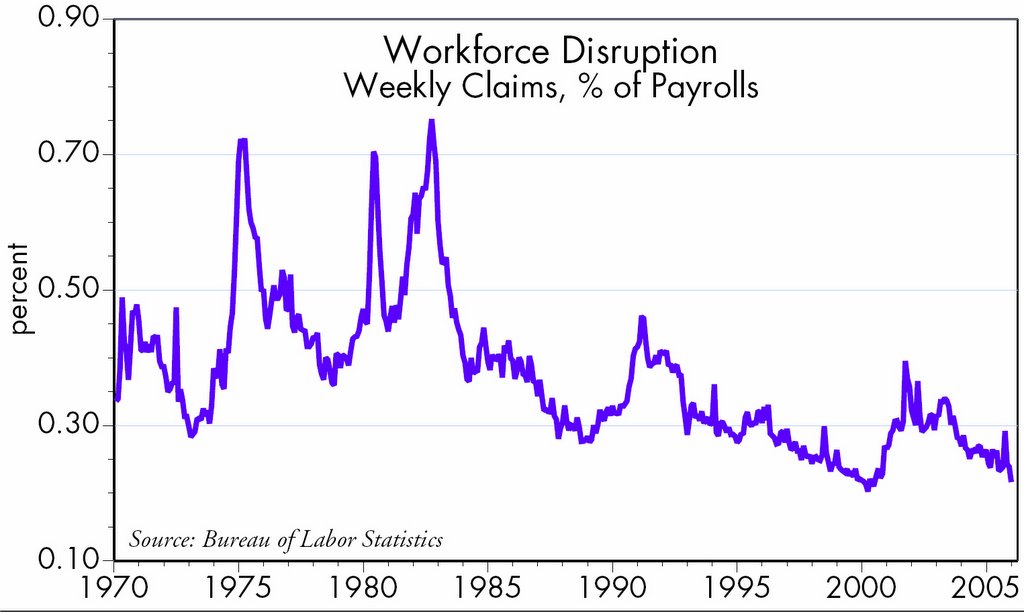

The jobs market by this measure is almost as healthy as it was in the late 1990s. Comparing the level of claims to the size of the workforce (below), we see that things are quite healthy indeed. The ratio was only briefly lower in the first half of 2000, when the economy was doing so well that the Fed was concerned about overheating. The real Fed funds rate peaked just short of 5% by the end of that year and a recession followed shortly thereafter.

This time things are different. The bond market seems convinced that economic growth will be moderate enough to allow the Fed to stop raising rates after one or two more hikes. But if the labor market continues to improve, before the year is over the Fed's models could be signalling the need for more tightening (too many people working means a very tight labor market that could supposedly feed into higher inflation). Continued above-trend economic growth would also raise the level of Fed concern.

The backdrop of asset prices is also a key difference. In 2000, gold was falling, all commodities were falling, and the dollar was rising. Today gold has surged to $550, energy prices have surged, nonenergy industrial commodities are reaching all-time highs, the dollar is almost 25% lower than its 2000 high, and the real Fed funds rate is only slightly higher than 2%. There is a lot of potential for the Fed to throw the market a curve ball, considering that several indicators are in or are approaching uncomfortable territory (e.g., the tightening jobs market, economic growth that has exceeded potential growth for 10 quarters, the price of gold, commodities, the dollar). For the funds rate to be 4.5% at year end, as the market currently expects, requires these variables to align just so, for a perfect soft landing. I'd have to say I agree with Greenspan's recent remarks to the effect that the bond market is remarkably calm in the face of so much potential uncertainty.

If I had to pick the most bullish indicator of the economy's health, this would be it. Taxes paid to the federal government in 2005 were 14% higher than in 2004. It is undeniably the case that corporate profits, personal incomes, and capital gains realizations are very strong, much stronger than anyone would have expected. Government statistics don't always pick up everything going on in the economy, but when tax revenues surge like this, you can be sure that the economy is very healthy. Even though federal revenues grew a robust 8.1% last year, the budget deficit fell from $400 billion to $320 billion, a mere 2.5% of GDP.

First-time unemployment claims rose last week, but the 4-week average remains in a declining trend, as the chart (below) shows.

The jobs market by this measure is almost as healthy as it was in the late 1990s. Comparing the level of claims to the size of the workforce (below), we see that things are quite healthy indeed. The ratio was only briefly lower in the first half of 2000, when the economy was doing so well that the Fed was concerned about overheating. The real Fed funds rate peaked just short of 5% by the end of that year and a recession followed shortly thereafter.

This time things are different. The bond market seems convinced that economic growth will be moderate enough to allow the Fed to stop raising rates after one or two more hikes. But if the labor market continues to improve, before the year is over the Fed's models could be signalling the need for more tightening (too many people working means a very tight labor market that could supposedly feed into higher inflation). Continued above-trend economic growth would also raise the level of Fed concern.

The backdrop of asset prices is also a key difference. In 2000, gold was falling, all commodities were falling, and the dollar was rising. Today gold has surged to $550, energy prices have surged, nonenergy industrial commodities are reaching all-time highs, the dollar is almost 25% lower than its 2000 high, and the real Fed funds rate is only slightly higher than 2%. There is a lot of potential for the Fed to throw the market a curve ball, considering that several indicators are in or are approaching uncomfortable territory (e.g., the tightening jobs market, economic growth that has exceeded potential growth for 10 quarters, the price of gold, commodities, the dollar). For the funds rate to be 4.5% at year end, as the market currently expects, requires these variables to align just so, for a perfect soft landing. I'd have to say I agree with Greenspan's recent remarks to the effect that the bond market is remarkably calm in the face of so much potential uncertainty.

posted by David M Gordon | 12:02 AM

![]()

<< Home