Productivity slows, inflation picks up; Scylla and Charybdis

The following commentary is by Scott Grannis, Chief Economist at Western Asset Management.

-- David M Gordon / The Deipnosophist

================================

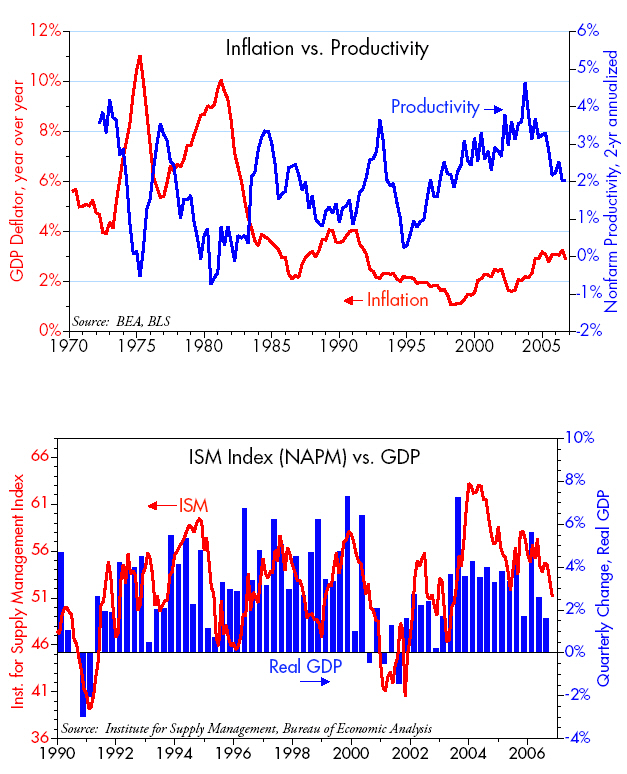

Nonfarm productivity was unchanged in the third quarter, which is not surprising since the economy grew at about the same rate (1.6%) as the growth in employment. This is a volatile series, however, posting numbers in the range of -0.5% to +10% over the past three years. But as the chart shows, the two-year trend in productivity has slowed rather significantly from the 3% or so pace we observed in the 2002-2004 period. Averaging 2% over the past two years, productivity is now right around its long-term average.

[click on image to enlarge]I have argued for several years that accommodative monetary policy would result in an upward drift in inflation, and higher inflation, by restoring pricing power, would take the edge off productivity (it's a lot easier to raise prices than it is to cut costs). Slower growth in productivity would then drive a "downshifting" in the economy's growth potential. And here we are. Inflation has risen from 1% to 3%, and productivity has declined. From mid-2003 to mid-2006 the economy grew 3.5-4.0%, and over the next few years it is likely to grow in a 2.5-3.0% range, assuming no further declines in productivity and employment growth of roughly 1.5%.

[click on image to enlarge]I have argued for several years that accommodative monetary policy would result in an upward drift in inflation, and higher inflation, by restoring pricing power, would take the edge off productivity (it's a lot easier to raise prices than it is to cut costs). Slower growth in productivity would then drive a "downshifting" in the economy's growth potential. And here we are. Inflation has risen from 1% to 3%, and productivity has declined. From mid-2003 to mid-2006 the economy grew 3.5-4.0%, and over the next few years it is likely to grow in a 2.5-3.0% range, assuming no further declines in productivity and employment growth of roughly 1.5%.

The ISM manufacturing survey released yesterday squares with a reduced growth outlook. The manufacturing sector is still healthy, but the index has slipped enough to warrant a 2-3% growth expectation for the economy as a whole.

The Fed's output gap model of inflation is probably assuming that the economy's potential growth rate has slipped to just under 3%, so the Fed would view 2.5-3% growth as nonthreatening. But for the foreseeable future, the Fed is likely to be steering a course between the Scylla of 3% core inflation (above its target) and the Charybdis of a weaker economy (something the Fed finds very hard to resist). The Fed will be betting that any tendency toward slower growth will have the silver lining of reducing the inflation threat, thus obviating the need for policy shifts.

Meanwhile, the market is assuming that the Fed will be forced to cut rates three times next year in order to avoid the risk of a weaker economy, and it is assuming that core inflation pressures will decline. But risks remain: gold is rising, the dollar is falling, and nonenergy commodity prices are hitting new highs, suggesting that inflation pressures are not yet declining; tax revenues and profits remain robust, energy prices have dropped, mortgage rates have reversed much of their earlier rise, swap spreads are down, and equity markets are up, suggesting that the outlook for growth has brightened on the margin.

-- David M Gordon / The Deipnosophist

================================

Nonfarm productivity was unchanged in the third quarter, which is not surprising since the economy grew at about the same rate (1.6%) as the growth in employment. This is a volatile series, however, posting numbers in the range of -0.5% to +10% over the past three years. But as the chart shows, the two-year trend in productivity has slowed rather significantly from the 3% or so pace we observed in the 2002-2004 period. Averaging 2% over the past two years, productivity is now right around its long-term average.

[click on image to enlarge]I have argued for several years that accommodative monetary policy would result in an upward drift in inflation, and higher inflation, by restoring pricing power, would take the edge off productivity (it's a lot easier to raise prices than it is to cut costs). Slower growth in productivity would then drive a "downshifting" in the economy's growth potential. And here we are. Inflation has risen from 1% to 3%, and productivity has declined. From mid-2003 to mid-2006 the economy grew 3.5-4.0%, and over the next few years it is likely to grow in a 2.5-3.0% range, assuming no further declines in productivity and employment growth of roughly 1.5%.

[click on image to enlarge]I have argued for several years that accommodative monetary policy would result in an upward drift in inflation, and higher inflation, by restoring pricing power, would take the edge off productivity (it's a lot easier to raise prices than it is to cut costs). Slower growth in productivity would then drive a "downshifting" in the economy's growth potential. And here we are. Inflation has risen from 1% to 3%, and productivity has declined. From mid-2003 to mid-2006 the economy grew 3.5-4.0%, and over the next few years it is likely to grow in a 2.5-3.0% range, assuming no further declines in productivity and employment growth of roughly 1.5%.The ISM manufacturing survey released yesterday squares with a reduced growth outlook. The manufacturing sector is still healthy, but the index has slipped enough to warrant a 2-3% growth expectation for the economy as a whole.

The Fed's output gap model of inflation is probably assuming that the economy's potential growth rate has slipped to just under 3%, so the Fed would view 2.5-3% growth as nonthreatening. But for the foreseeable future, the Fed is likely to be steering a course between the Scylla of 3% core inflation (above its target) and the Charybdis of a weaker economy (something the Fed finds very hard to resist). The Fed will be betting that any tendency toward slower growth will have the silver lining of reducing the inflation threat, thus obviating the need for policy shifts.

Meanwhile, the market is assuming that the Fed will be forced to cut rates three times next year in order to avoid the risk of a weaker economy, and it is assuming that core inflation pressures will decline. But risks remain: gold is rising, the dollar is falling, and nonenergy commodity prices are hitting new highs, suggesting that inflation pressures are not yet declining; tax revenues and profits remain robust, energy prices have dropped, mortgage rates have reversed much of their earlier rise, swap spreads are down, and equity markets are up, suggesting that the outlook for growth has brightened on the margin.

Labels: Economics

posted by David M Gordon | 3:23 AM

![]()

<< Home