Housing downturn now very obvious + Capex still strong

-- David M Gordon / The Deipnosophist

================================

Begin Scott Grannis...

Housing downturn now very obvious

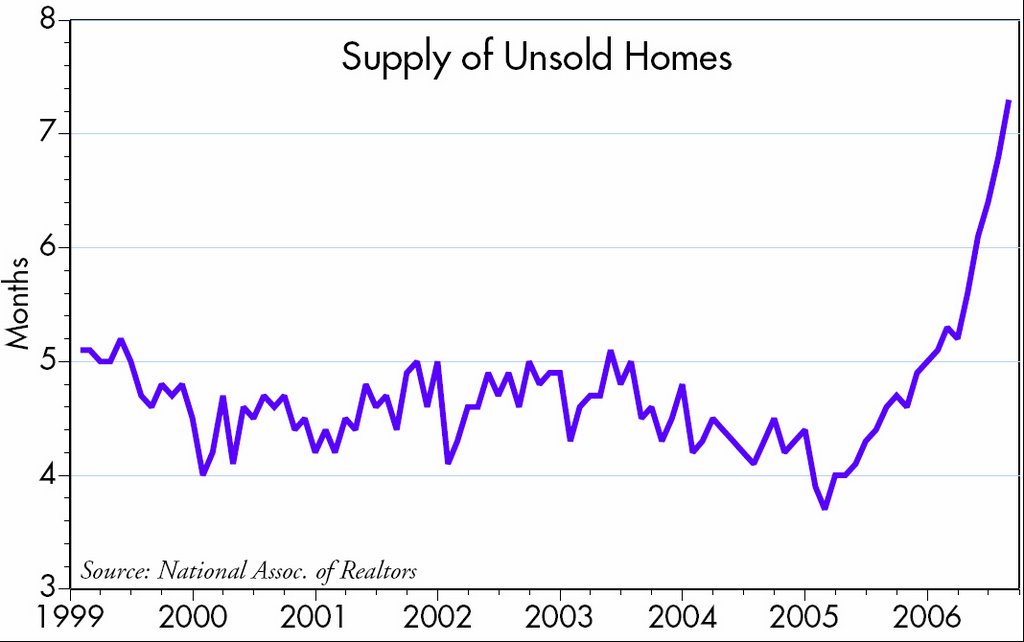

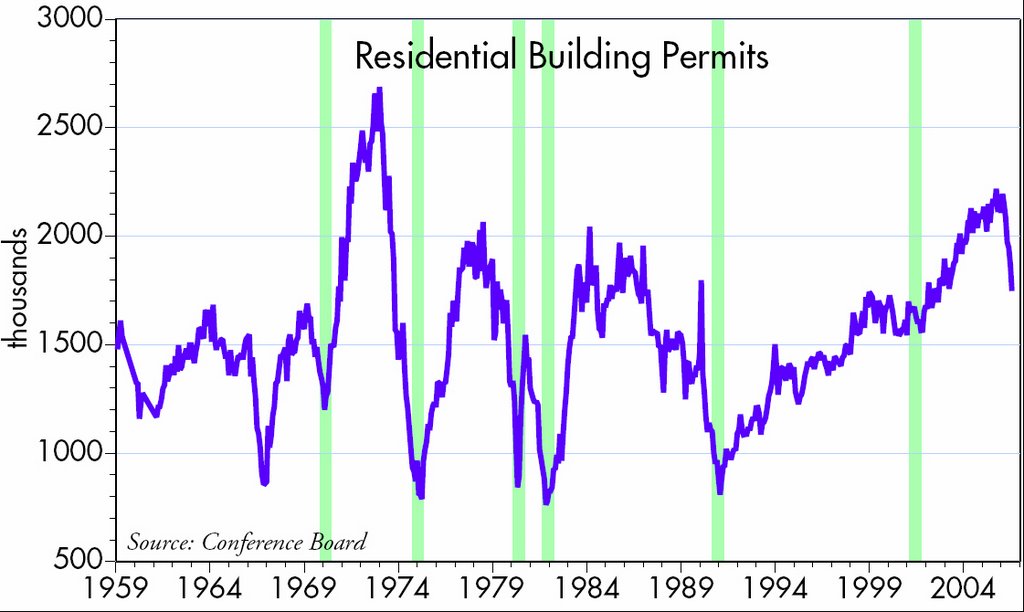

These three charts make it pretty clear that we are in the midst of a full-blown downturn in the U.S. housing market. The financial markets have been waiting for this for quite some time, and it's now no longer a rumor but an established fact. The inventory of unsold homes has almost doubled since the peak of the market early last year. An index of home builders' confidence has dropped by almost half. Residential building permits are down just over 20% from their high. The other shoe that has yet to drop is housing prices, which on average have stopped rising, according to the National Assoc. of Realtors, but will most likely fall in the months to come; the only question now is how far prices will eventually decline.

The trigger for the "bursting" of the housing bubble appears to be higher mortgage rates, which earlier this year were 140 basis points higher than their lows of last summer. Housing prices may have been "fair" at the mortgage rates that prevailed a year ago, but higher rates have tipped the affordability scales in the direction of lower prices, and it's now a buyer's market. With the Fed on the sidelines, the bond market has breathed a sigh of relief, and 30-year fixed mortgage rates have fallen 40 bps from their June highs. Adjustable mortgage rates are up 140 bps from the levels of last summer, but have been relatively stable for the past several months. Refinancing activity has actually picked up in the past month, and applications for new mortgages have stopped falling. So the news is not all bad, but it's hard to imagine that housing won't continue to deteriorate over the next year.

As the second and third charts suggest, a housing downturn on the scale of the one we're witnessing could be signalling a recession, and that would be the third shoe to drop, as it were. However, there are a number of indicators that are still flashing very healthy signals for the economy: tax revenues are still flooding into state and federal treasuries; corporate profits are at all-time highs; weekly claims for unemployment are still trending down; the real Fed funds rate, currently a bit less than 2%, is far below the 4% that has preceded every recession for the past 40 years; the yield curve is not inverted; tax burdens are not particularly high; business capex is still rising; the ISM index is still a healthy 55, far above the 45 which typically signals a recession; and industrial production is accelerating both here and abroad. It's also important to note that residential construction is a much smaller part of the economy today than it has been in the past: building permits today are about the same as they were in 1984, but the economy today is twice the size it was then.

The housing slowdown will certainly contribute to slow the economy, but probably not enough to qualify as a recession. And even if prices decline significantly, it wouldn't necessarily be the end of the world. Recall the massive wealth losses that the economy has sustained in the past without falling into a recession: the 33% crash in the stock market in October 1987; the real estate crash of 1990-95, when prices fell 25-30% in many markets; and the 30% decline in the S&P 500 in 2002.

[click on images to enlarge]

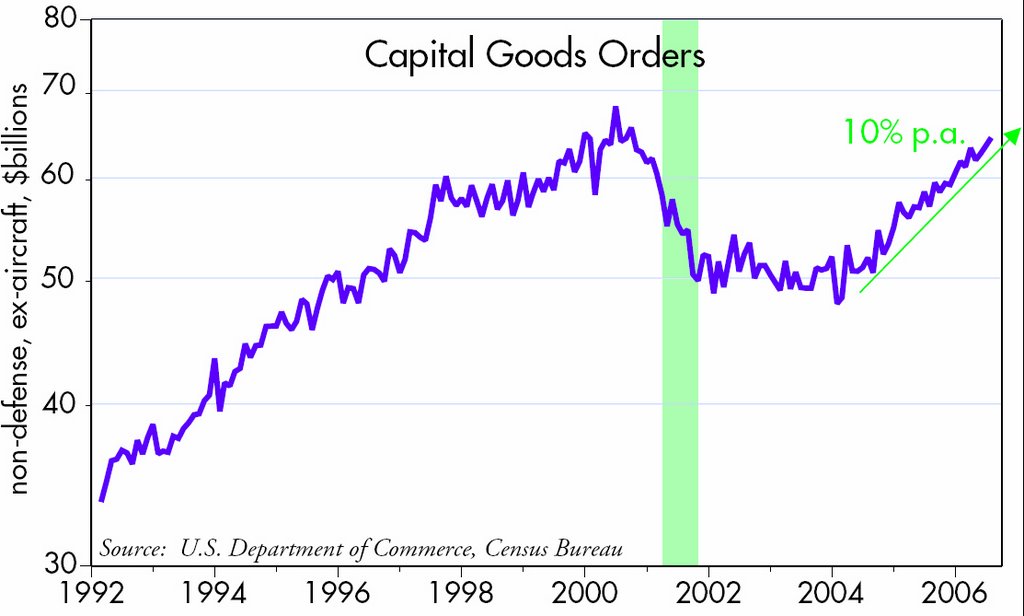

Capex still strong

Housing may be tanking, but the business community remains optimistic about the future. Capital spending has been growing at a 10% pace for the past two years, with no sign yet of any slowdown. Corporate profits have surged, and the money is being put to work, laying the foundation for ongoing productivity gains and economic growth in the years to come. Indeed, corporations have only just begun to tap the mountain of cash that they have accumulated in recent years. After tax corporate profits have doubled since 2000, but capital spending has only just returned to the levels of 2000. This equates to a substantial source of reserve energy that can help offset the weakness coming from the housing sector.

[click on image to enlarge]

[click on image to enlarge]Labels: Economics

posted by David M Gordon | 5:52 AM

![]()

<< Home