Jobs and Oil

The following comments and graphics courtesy of Scott Grannis, Chief Economist at Western Asset Management...

Jobs:

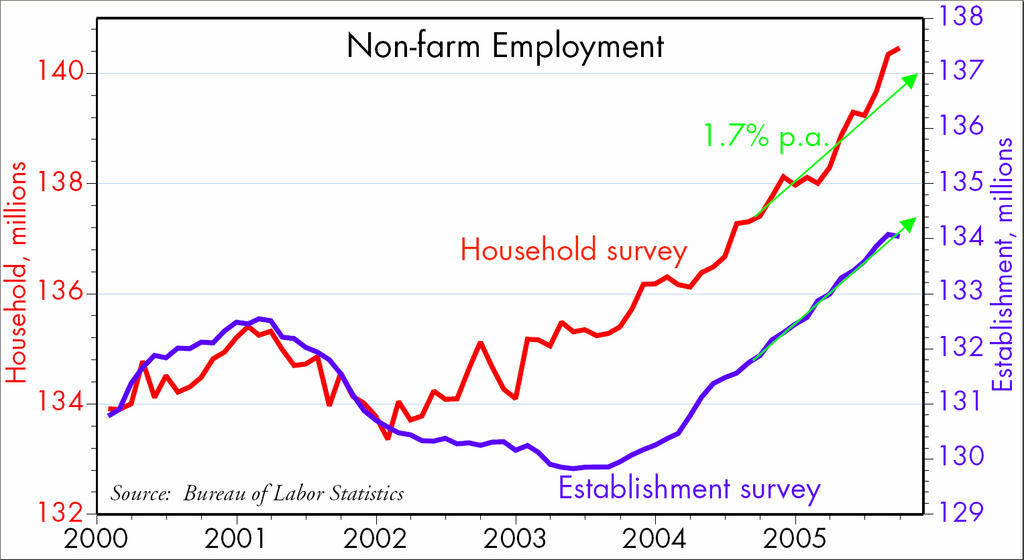

"According to the establishment survey, jobs fell by 35,000 last month instead of the expected 150,000. According to the household survey, however, jobs rose by 116,000. As the chart shows, and if we assume that the household survey is better at picking up changing trends than the establishment survey, jobs growth was accelerating in the months leading up to the Katrina disaster, and that explains why today's numbers were better than expected. Over the past year, the household survey has reflected jobs growth averaging about 250,000 per month, or 2.2% per year, whereas the establishment survey was showing growth of about 200,000 per month, or 1.7% per year.

"On balance, then, it seems that the economy was on more solid ground than many thought, and should therefore be able to absorb the Katrina damage without too much difficulty."

Oil:

"In order to produce a unit of output, the U.S. economy today requires about one-half as much oil as it did in 1970.

"The U.S. economy's oil efficiency, measured in terms of oil consumed per unit of output, has improved at the rate of about 2% per year since 1970. In other words, oil consumption per unit of output has fallen by about 2% per year. Oil efficiency rose about 3.5% per year from 1979 to 1989, a period during which real oil prices were historically high. Since 1990, oil efficiency has increased at about 1.5% per year, a period during which real oil prices have been on average much lower than they were in the early 1980s.

"High real oil prices, such as we saw in the late 1970s and early 1980s, were the likely cause of rapid gains in oil efficiency in the 1980s.

"The real price of oil today is at approximately the same level as it was in 1979, but the economy requires about 45% less oil today to produce a unit of output. Adjusting for the economy's oil dependence, we might say that real oil prices today are about half of what they were in 1979-80. The economy grew very strongly (4.8% per year) in the 1982-1986 period, despite oil prices that in "adjusted" terms were higher than they are today.

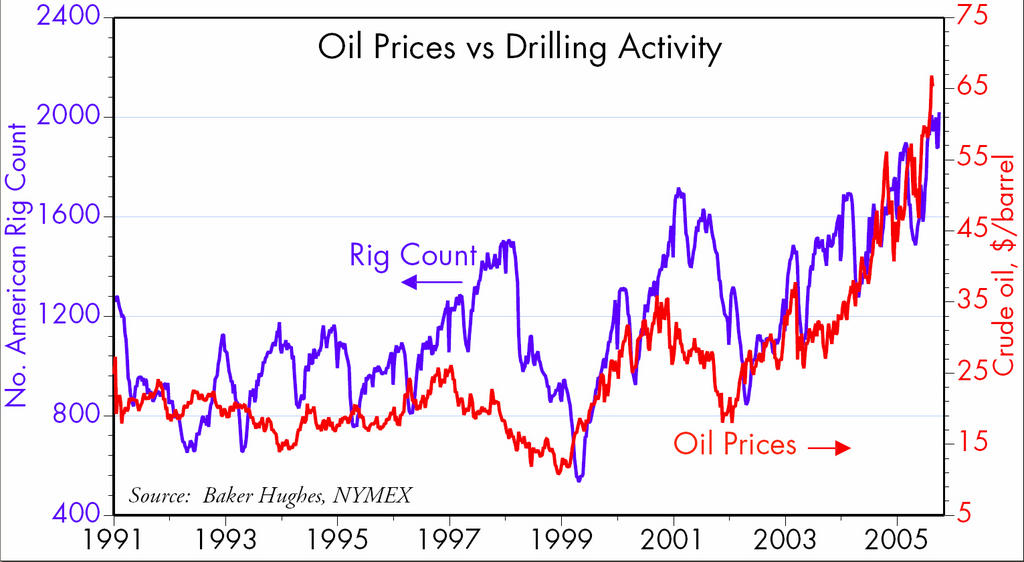

"Significant changes in oil prices are a good leading indicator of drilling activity. Since oil prices started rising in 1999, the North American rig count has roughly tripled. The U.S. rig count has doubled since early 2002. It takes several years at least for increased drilling activity to result in higher production.

"High oil prices do not suck money out of the U.S. economy. Oil producers cannot spend their "windfall" revenues as fast as oil prices are rising. Thus, most of the extra spending in the U.S. on oil is simply recycled by oil producers back into the U.S. financial markets. In a sense, rising gasoline prices make it easier for homeowners to refinance their mortgages.

What this suggests:

"Adjusting for inflation and the economy's oil dependence, oil prices are high, but not exceedingly so in an historical context. Current oil prices are not by themselves likely to put a serious dent in the economy's ability to grow. Indeed, high oil prices are better thought of as a barometer of how strong the economy is. Still, today's oil prices are probably high enough to result in increased conservation and substitution efforts on the margin, resulting in a softening of U.S. demand for oil in the years to come. This is probably true for most industrialized economies. Chinese demand for oil, however, is likely to continue to be very strong, even though their energy efficiency is much lower than ours and could improve significantly in the years to come. If China's oil efficiency were to improve to current U.S. levels, and its economy were to grow by 10% per year, Chinese demand for oil in 20 years would still more than triple, to eclipse current oil consumption in the U.S.

"Increased exploration activity is likely to result in substantial increases in oil supplies in the years to come. Whether and when this will exceed the world's increased demand for oil, thus bringing prices down, is the $64,000 question.

"Since the Federal Reserve is still somewhat accommodative (per their own admission and judging by the relatively weak dollar, rising gold prices, rising commodity prices, rising real estate prices and low real yields), oil prices today likely contain some "inflation component" in the sense that the demand for oil is being boosted by the desire of producers and consumers to hold higher-than-normal inventories of oil. At the same time, accommodative money policy means that it is relatively easy for businesses to "pass on" higher energy costs to consumers.

"For the next year or so, oil prices could remain at current levels without causing significant harm to the U.S. or global economy. However, higher oil prices are likely to find their way into core measures of inflation, with the result that U.S. interest rates are likely to be higher at some point than the market is currently estimating."

Jobs:

"According to the establishment survey, jobs fell by 35,000 last month instead of the expected 150,000. According to the household survey, however, jobs rose by 116,000. As the chart shows, and if we assume that the household survey is better at picking up changing trends than the establishment survey, jobs growth was accelerating in the months leading up to the Katrina disaster, and that explains why today's numbers were better than expected. Over the past year, the household survey has reflected jobs growth averaging about 250,000 per month, or 2.2% per year, whereas the establishment survey was showing growth of about 200,000 per month, or 1.7% per year.

"On balance, then, it seems that the economy was on more solid ground than many thought, and should therefore be able to absorb the Katrina damage without too much difficulty."

Oil:

"In order to produce a unit of output, the U.S. economy today requires about one-half as much oil as it did in 1970.

"The U.S. economy's oil efficiency, measured in terms of oil consumed per unit of output, has improved at the rate of about 2% per year since 1970. In other words, oil consumption per unit of output has fallen by about 2% per year. Oil efficiency rose about 3.5% per year from 1979 to 1989, a period during which real oil prices were historically high. Since 1990, oil efficiency has increased at about 1.5% per year, a period during which real oil prices have been on average much lower than they were in the early 1980s.

"High real oil prices, such as we saw in the late 1970s and early 1980s, were the likely cause of rapid gains in oil efficiency in the 1980s.

"The real price of oil today is at approximately the same level as it was in 1979, but the economy requires about 45% less oil today to produce a unit of output. Adjusting for the economy's oil dependence, we might say that real oil prices today are about half of what they were in 1979-80. The economy grew very strongly (4.8% per year) in the 1982-1986 period, despite oil prices that in "adjusted" terms were higher than they are today.

"Significant changes in oil prices are a good leading indicator of drilling activity. Since oil prices started rising in 1999, the North American rig count has roughly tripled. The U.S. rig count has doubled since early 2002. It takes several years at least for increased drilling activity to result in higher production.

"High oil prices do not suck money out of the U.S. economy. Oil producers cannot spend their "windfall" revenues as fast as oil prices are rising. Thus, most of the extra spending in the U.S. on oil is simply recycled by oil producers back into the U.S. financial markets. In a sense, rising gasoline prices make it easier for homeowners to refinance their mortgages.

What this suggests:

"Adjusting for inflation and the economy's oil dependence, oil prices are high, but not exceedingly so in an historical context. Current oil prices are not by themselves likely to put a serious dent in the economy's ability to grow. Indeed, high oil prices are better thought of as a barometer of how strong the economy is. Still, today's oil prices are probably high enough to result in increased conservation and substitution efforts on the margin, resulting in a softening of U.S. demand for oil in the years to come. This is probably true for most industrialized economies. Chinese demand for oil, however, is likely to continue to be very strong, even though their energy efficiency is much lower than ours and could improve significantly in the years to come. If China's oil efficiency were to improve to current U.S. levels, and its economy were to grow by 10% per year, Chinese demand for oil in 20 years would still more than triple, to eclipse current oil consumption in the U.S.

"Increased exploration activity is likely to result in substantial increases in oil supplies in the years to come. Whether and when this will exceed the world's increased demand for oil, thus bringing prices down, is the $64,000 question.

"Since the Federal Reserve is still somewhat accommodative (per their own admission and judging by the relatively weak dollar, rising gold prices, rising commodity prices, rising real estate prices and low real yields), oil prices today likely contain some "inflation component" in the sense that the demand for oil is being boosted by the desire of producers and consumers to hold higher-than-normal inventories of oil. At the same time, accommodative money policy means that it is relatively easy for businesses to "pass on" higher energy costs to consumers.

"For the next year or so, oil prices could remain at current levels without causing significant harm to the U.S. or global economy. However, higher oil prices are likely to find their way into core measures of inflation, with the result that U.S. interest rates are likely to be higher at some point than the market is currently estimating."

posted by David M Gordon | 5:15 PM

![]()

<< Home