Japanese deflation - end of an era

The following guest commentary is from Scott Grannis, Chief Economist at Western Asset Management...

-- David M Gordon / The Deipnosophist

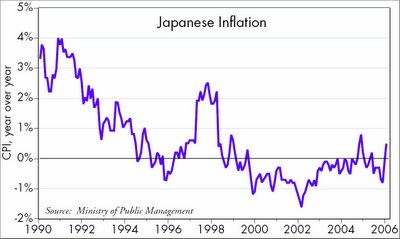

Japanese deflation has been vanquished. Japan's CPI rose 0.5% in the 12 months ended January, a testimony to the power of monetary policy to end even apparently intractable deflation. At the root of Japan's deflation was the Bank of Japan's massive monetary tightening which first became evident when the yen soared against the dollar, rising from 250 in 1985 to 120 by late 1987. It was also reflected in the yen's huge appreciation relative to gold, with yen gold prices plunging from 70,000 yen/oz. in 1987 to 30,000/oz. in 2000. As a result of tight monetary policy from 1988 to 2000, Japanese bank reserves were unchanged for 13 years, putting its economy on a what was effectively a starvation monetary diet.

The BoJ didn't get serious about ending deflation until 2001. "Quantitative easing" then force-fed money into the banking system, with the result that bank reserves skyrocketed 500% from 2001 to 2004. With the typical lags from policy to the economy, it took a few years for expansive monetary policy to take effect, but it is now finally working to push prices higher.

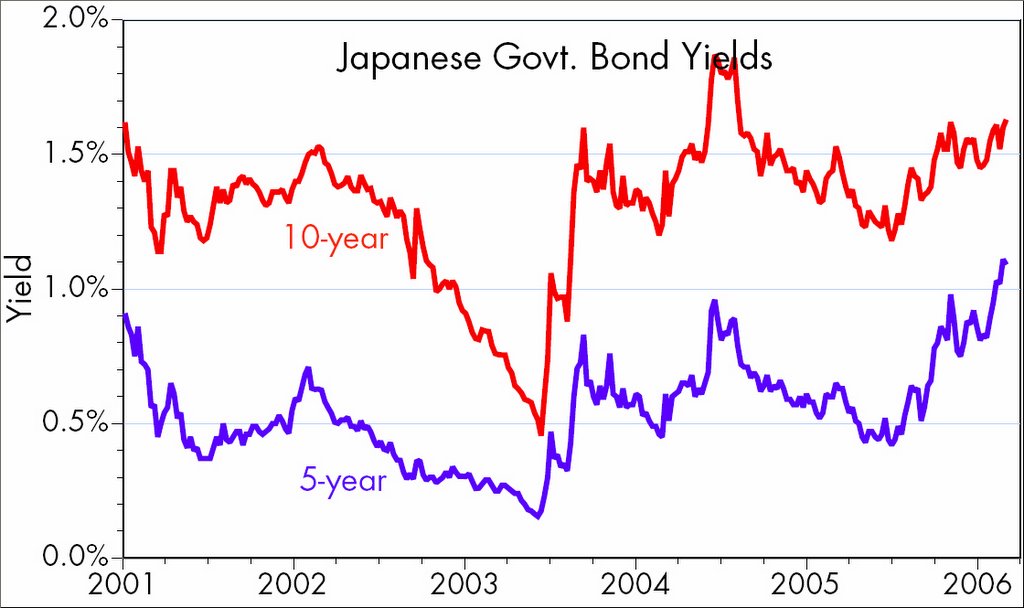

Bond yields are almost certain to rise significantly from current levels, and the BoJ is equally likely to raise its policy rate substantially above zero in the next year or two. Whether the BoJ formally ends quantitative easing in the next month or two is not really as important as the fact that it has accomplished its goal. Higher interest rates are almost inevitable, but they will not be bad news for the economy, and could even help to stimulate it. Rising yields are ultimately driven by a rising price level, and the end of deflation removes one of the sources of Japan's chronically sluggish growth by encouraging consumers to spend their money instead of hoarding it.

Japan's industrial production now stands at a new all-time high, only recently surpassing the prior high set all the way back in 1991. A 15-year economic stagnation has come to an end, and not surprisingly, Japan's stock market has doubled in the past three years, soaring 45% since last May. What's good for Japan is good for the world, since a more vibrant and spendthrift Japan translates into stronger demand for the world's goods and services. Moreover, an aging Japan will be spending more and more of the savings its people have salted away throughout the world.

Will higher interest rates boost the yen as many seem to think? It will be quite some time before higher interest rates in Japan equate to restrictive monetary policy. For now, higher rates will simply offset higher prices; real interest rates shouldn't change by much. By raising rates, the BoJ will only be offsetting declining demand for yen as deflationary hoarding of yen is gradually replaced by a more normal velocity of circulation. One fundamental limitation on the yen's potential strength is the fact that even though the economy is once again expanding and prices are once again rising, Japan's shrinking population and strict limits on immigration condemn its workforce to decline and that severly limits the ability of the economy to grow. Henceforth, Japanese growth will be all about productivity, not physical expansion.

-- David M Gordon / The Deipnosophist

Japanese deflation has been vanquished. Japan's CPI rose 0.5% in the 12 months ended January, a testimony to the power of monetary policy to end even apparently intractable deflation. At the root of Japan's deflation was the Bank of Japan's massive monetary tightening which first became evident when the yen soared against the dollar, rising from 250 in 1985 to 120 by late 1987. It was also reflected in the yen's huge appreciation relative to gold, with yen gold prices plunging from 70,000 yen/oz. in 1987 to 30,000/oz. in 2000. As a result of tight monetary policy from 1988 to 2000, Japanese bank reserves were unchanged for 13 years, putting its economy on a what was effectively a starvation monetary diet.

The BoJ didn't get serious about ending deflation until 2001. "Quantitative easing" then force-fed money into the banking system, with the result that bank reserves skyrocketed 500% from 2001 to 2004. With the typical lags from policy to the economy, it took a few years for expansive monetary policy to take effect, but it is now finally working to push prices higher.

Bond yields are almost certain to rise significantly from current levels, and the BoJ is equally likely to raise its policy rate substantially above zero in the next year or two. Whether the BoJ formally ends quantitative easing in the next month or two is not really as important as the fact that it has accomplished its goal. Higher interest rates are almost inevitable, but they will not be bad news for the economy, and could even help to stimulate it. Rising yields are ultimately driven by a rising price level, and the end of deflation removes one of the sources of Japan's chronically sluggish growth by encouraging consumers to spend their money instead of hoarding it.

Japan's industrial production now stands at a new all-time high, only recently surpassing the prior high set all the way back in 1991. A 15-year economic stagnation has come to an end, and not surprisingly, Japan's stock market has doubled in the past three years, soaring 45% since last May. What's good for Japan is good for the world, since a more vibrant and spendthrift Japan translates into stronger demand for the world's goods and services. Moreover, an aging Japan will be spending more and more of the savings its people have salted away throughout the world.

Will higher interest rates boost the yen as many seem to think? It will be quite some time before higher interest rates in Japan equate to restrictive monetary policy. For now, higher rates will simply offset higher prices; real interest rates shouldn't change by much. By raising rates, the BoJ will only be offsetting declining demand for yen as deflationary hoarding of yen is gradually replaced by a more normal velocity of circulation. One fundamental limitation on the yen's potential strength is the fact that even though the economy is once again expanding and prices are once again rising, Japan's shrinking population and strict limits on immigration condemn its workforce to decline and that severly limits the ability of the economy to grow. Henceforth, Japanese growth will be all about productivity, not physical expansion.

posted by David M Gordon | 6:20 PM

![]()

<< Home