Katrina's wake - Energy and infrastructure

The cogent analysis that follows is by Harry Wilker, a regular visitor at the table of The Deipnosophist...

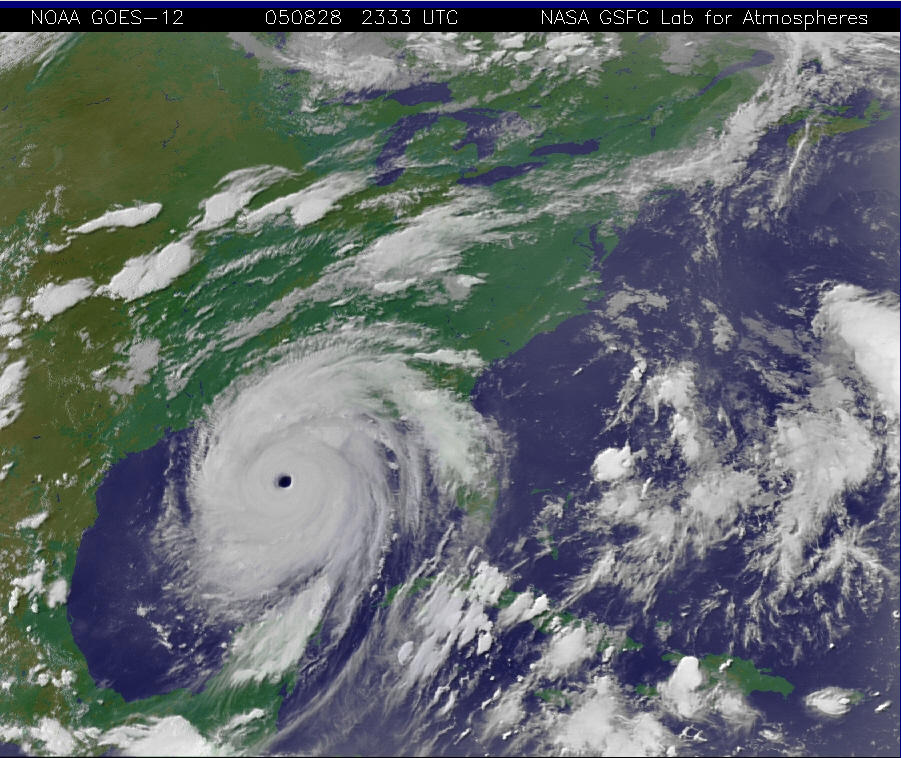

We are all hearing now about the human devastation in the Gulf area. I have no information to add to what you undoubtedly already know. Infrastructure issues are hardly as critical as the life-threatening catastrophe in New Orleans and elsewhere, but I've also been monitoring infrastructure issues today. For those interested this is what I've collected.

ENERGY

95% of oil production in the gulf is shut down and 88% of the natural gas production.

10 refineries are shut down representing 10% of the US refining capacity, including refineries owned by Marathon, Valero, Murphy, Conoco Phillips and Shell Chemical. 4 others are running at reduced capacity.

So far, only 1 of about 4000 oil production platforms has been reported as destroyed (owned by Newfield Exploration). 7 drilling rigs are adrift: one is lost (Diamond Offshore) one is grounded (Gulf Santa Fe) and one is listing (also Global Santa Fe) 3 have been secured (Diamond, Noble and Ensco). I don't know the status of the others.

Chevron's refinery - the second largest in the US - has yet to be evaluated as teams have not been able to reach the facility yet due to flooding.

The LOOP sustained little damage and is capable of restarting the offloading of oil within hours of power restoration. The road leading to Port Fourchon is passable.

The Henry Hub which is the offloading facility for natural gas is functioning normally.

The condition of the pipelines leading from the gulf to areas from Denver to the East Coast is unknown.

PORTS AND WATERWAYS

The Port of New Orleans is completely shut down. The Coast Guard has closed all ports on the Mississippi for at least several days.

There are no estimates as to obstructions or silt in the water either in the rivers or the coastal waters. The LOOP indicated that it may be impossible for tankers to reach the offloading point and that the area around the LOOP might have to be dredged. They simply didn't know yet.

POWER

The two major utilities in the area, Entergy and Southern Co, suffered extensive damage to transmission systems. Entergy reported that it might be a month before power is fully restored, though they will focus first on such things as hospitals and infrastructure.

Here's my take on what this all means:

Restarting oil flow to refineries is probably less dependent on physical damage to pipelines and port facilities, than it is on three factors:

• restoration of power,

• clearing shipping lanes and other waters that support the offloading and shipping of oil, and

• availability of personnel.

This last one may be toughest of all, given the devastation and flooding. How quickly will people be able to lift their focus from the immediate family and/or shelter to report to work and how long before they can get there.

I continue to think that the energy bottleneck is the refineries. Most telling to me is what Valero said. They said that they suffered no significant damage and that they could be back in operation two weeks after power is restored. If that's the case for a refinery that didn't suffer damage how long will it be before refineries that suffered damage will be back in operations. One analyst estimated that if Chevron's very large refinery should be unable to function it alone might account for a $1 a gallon spike in gasoline prices. It also pays to remember that the far less extensive damage that Ivan inflicted last year was not totally restored until almost a year later. Of course much of it was restored much earlier but that is how long it took to complete all repairs on all facilities. Katrina is likely to dwarf Ivan in the amount of damage that is inflicted.

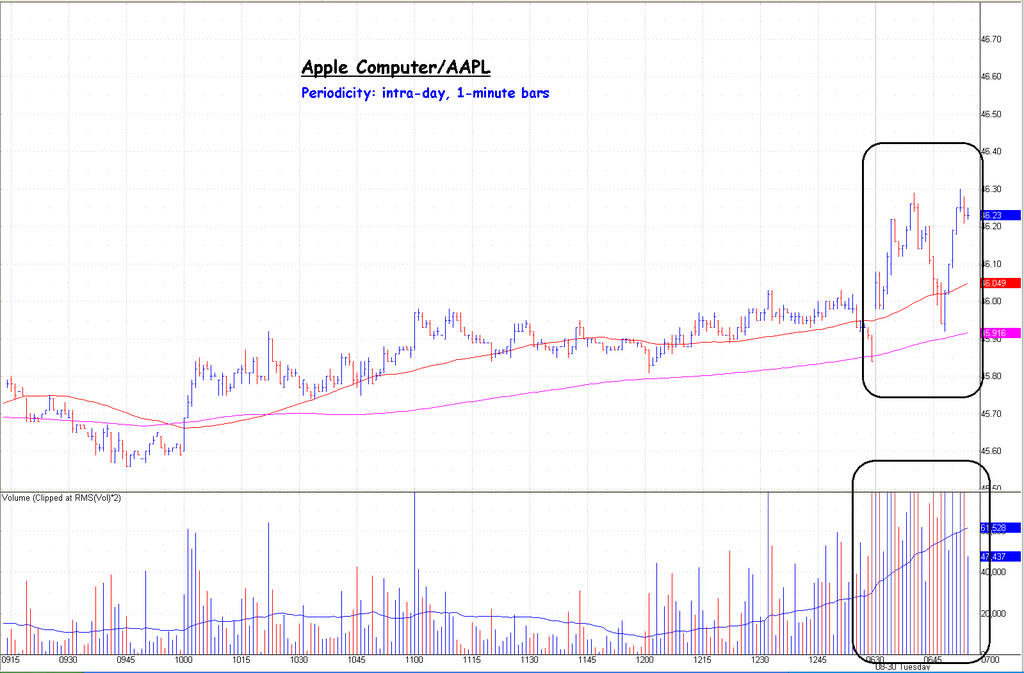

The media has largely focused on the rise of crude oil prices since the storm hit, but the rise in natural gas and refined products is much worse. Since Friday's close on the futures market:

Crude up 5.6%

Heating Oil up 14.5%

Unleaded Gas up 18.7%

Natural Gas up 23.2%

All these products are up even more in the after-hours electronic market apparently in response to the proposed evacuation of New Orleans. Several analysts suggested today that shortages of refined products could develop within the next week in the Eastern half of the country.

'nuff said. This is going to get very ugly before it gets better. I can't even imagine what it would be like to be stuck in New Orleans tonight.

We are all hearing now about the human devastation in the Gulf area. I have no information to add to what you undoubtedly already know. Infrastructure issues are hardly as critical as the life-threatening catastrophe in New Orleans and elsewhere, but I've also been monitoring infrastructure issues today. For those interested this is what I've collected.

ENERGY

95% of oil production in the gulf is shut down and 88% of the natural gas production.

10 refineries are shut down representing 10% of the US refining capacity, including refineries owned by Marathon, Valero, Murphy, Conoco Phillips and Shell Chemical. 4 others are running at reduced capacity.

So far, only 1 of about 4000 oil production platforms has been reported as destroyed (owned by Newfield Exploration). 7 drilling rigs are adrift: one is lost (Diamond Offshore) one is grounded (Gulf Santa Fe) and one is listing (also Global Santa Fe) 3 have been secured (Diamond, Noble and Ensco). I don't know the status of the others.

Chevron's refinery - the second largest in the US - has yet to be evaluated as teams have not been able to reach the facility yet due to flooding.

The LOOP sustained little damage and is capable of restarting the offloading of oil within hours of power restoration. The road leading to Port Fourchon is passable.

The Henry Hub which is the offloading facility for natural gas is functioning normally.

The condition of the pipelines leading from the gulf to areas from Denver to the East Coast is unknown.

PORTS AND WATERWAYS

The Port of New Orleans is completely shut down. The Coast Guard has closed all ports on the Mississippi for at least several days.

There are no estimates as to obstructions or silt in the water either in the rivers or the coastal waters. The LOOP indicated that it may be impossible for tankers to reach the offloading point and that the area around the LOOP might have to be dredged. They simply didn't know yet.

POWER

The two major utilities in the area, Entergy and Southern Co, suffered extensive damage to transmission systems. Entergy reported that it might be a month before power is fully restored, though they will focus first on such things as hospitals and infrastructure.

Here's my take on what this all means:

Restarting oil flow to refineries is probably less dependent on physical damage to pipelines and port facilities, than it is on three factors:

• restoration of power,

• clearing shipping lanes and other waters that support the offloading and shipping of oil, and

• availability of personnel.

This last one may be toughest of all, given the devastation and flooding. How quickly will people be able to lift their focus from the immediate family and/or shelter to report to work and how long before they can get there.

I continue to think that the energy bottleneck is the refineries. Most telling to me is what Valero said. They said that they suffered no significant damage and that they could be back in operation two weeks after power is restored. If that's the case for a refinery that didn't suffer damage how long will it be before refineries that suffered damage will be back in operations. One analyst estimated that if Chevron's very large refinery should be unable to function it alone might account for a $1 a gallon spike in gasoline prices. It also pays to remember that the far less extensive damage that Ivan inflicted last year was not totally restored until almost a year later. Of course much of it was restored much earlier but that is how long it took to complete all repairs on all facilities. Katrina is likely to dwarf Ivan in the amount of damage that is inflicted.

The media has largely focused on the rise of crude oil prices since the storm hit, but the rise in natural gas and refined products is much worse. Since Friday's close on the futures market:

Crude up 5.6%

Heating Oil up 14.5%

Unleaded Gas up 18.7%

Natural Gas up 23.2%

All these products are up even more in the after-hours electronic market apparently in response to the proposed evacuation of New Orleans. Several analysts suggested today that shortages of refined products could develop within the next week in the Eastern half of the country.

'nuff said. This is going to get very ugly before it gets better. I can't even imagine what it would be like to be stuck in New Orleans tonight.

posted by David M Gordon | 7:14 PM

![]()