Zara Elis gets creative...

Zara says of this photo, "Here is my first blush rose of the season..."

[click photo to enlarge]

[click photo to enlarge]To which I say, "...'Tis a beauty -- subject and photo!"

posted by David M Gordon | 11:29 AM

![]()

Where the science of investing becomes an art of living

A private investor for 20+ years, I manage private portfolios and write about investing. You can read my market musings on three different sites: 1) The Deipnosophist, dedicated to teaching the market's processes and mechanics; 2) Investment Poetry, a subscription site dedicated to real time investment recommendations; and 3) Seeking Alpha, a combination of the other two sites with a mix of reprints from this site and all-original content. See you here, there, or the other site!

[click photo to enlarge]

[click photo to enlarge]To which I say, "...'Tis a beauty -- subject and photo!"

posted by David M Gordon | 11:29 AM

![]()

.jpg)

.jpg)

.jpg)

.jpg)

posted by David M Gordon | 7:11 AM

![]()

Cauff was a victim of "click fraud," the illicit manipulation of keyword-based advertising. In this case, the scam appeared straightforward - one company clicked on a rival's search engine ads to drive up its costs. More complex is a second type of bogus ad click that exploits a second form of PPC advertising: ads fed to Web sites - anything from personal blogs to the sites of major corporations - by search providers like Google, Yahoo!, LookSmart, and, soon, MSN. The search engine indexes the content of the Web site and matches it with a group of relevant ads. (The most familiar form is Google's AdSense program - the sets of links labeled ads by goooooogle that show up on pages across the Internet. The advertisements that appear on Google itself are part of a separate but related program called AdWords.) Thus, bloggers who write about their air-travel experiences and choose to host such ads may find links on their pages for JetNetworks and its brethren. If a blog visitor clicks on the ad, the search engine splits its fee with the blogger. Although these "affiliate" ads have been hugely successful for advertisers, search engines, and the host Web sites, the system creates an incentive for affiliates to cheat. "All you have to do to make some money is find a way to click the ad sent by Google or Yahoo! to your own Web page," says search marketing consultant Joseph Holcomb. "Click! - there's 10 bucks. Click! - there's 10 bucks. It goes on all the time."Click fraud is an important and growing problem. It afflicts consumers, advertisers, and the venue purveyors themselves (primarily, Google, Yahoo, and Microsoft/MSN). Google suffers the most abuse, largely because it is the King Kong of the savannah. However, Google, in addition to Yahoo and Microsoft, treat this problem very seriously. It even is possible that, in their reaction, they go too far; for example, publishers lose their AdSense licenses for the mere perception of an abuse.

posted by David M Gordon | 2:13 AM

![]()

"The rise of Google is a tale often told as a Silicon Valley classic. Two precocious Stanford grad-student nerds swept up in the fever of the Internet boom invent technology that profoundly changes the experience of the Web; they drop out and start a company (in a garage) that achieves iconic status; they stage a historic public offering, achieving vast wealth and fame... But beneath these familiar surface details, the Google story is more nuanced and compelling. It’s a story about the clash between youth and experience, more a messy ensemble drama than a simple buddy flick — one whose main characters have persistently deviated from any script, resulting in unexpected twists and turns that haven’t come to light until now."And it is funny. Comparatively lengthy, it makes for good reading material for the holiday-lengthened weekend.

posted by David M Gordon | 10:17 AM

![]()

"Though many of the services are free, Google will no doubt figure out a way to charge for some of them so it's not so dependent on advertising."I do not agree with each comment, however, as you will discover upon reading; nonetheless, the article is worthy of your attention.

posted by David M Gordon | 5:10 AM

![]()

"It was promising. If they only could be made to understand the concept of symbology, and of words, he might be able to start establishing a pidgin. If the boredom didn’t kill him first."

WORLDWIRED, p 313

Elizabeth Bear holds aloft the John W Campbell award for “Best New Writer” of 2005 in the genre of Science Fiction. (Congratulations to Elizabeth, and her Bantam Spectra editor, Anne Groell.)

Elizabeth Bear holds aloft the John W Campbell award for “Best New Writer” of 2005 in the genre of Science Fiction. (Congratulations to Elizabeth, and her Bantam Spectra editor, Anne Groell.)Upcoming books from Elizabeth include:

• A short story collection from Night Shade Press, The Chains that you Refuse;

• A fantasy duology from publisher, Ace/ROC, the Promethean Age novels, Blood and Iron and Whiskey and Water that will appear beginning in June 2006.

• Two standalone novels from Bantam Spectra, Carnival, a novel of Singularity, eco-terrorism, sexism, genocide, brinksmanship, art, intrigue -- and spies! And Undertow, a novel about a hit man, a conjure man, a fish boygirl, and a Woman with a Past.

Run, do not walk, to your nearest bookseller, buy (any of) these books, and then sit back and enjoy.

Labels: Humanities

posted by David M Gordon | 8:22 AM

![]()

[click image to enlarge]

[click image to enlarge]

posted by David M Gordon | 7:22 AM

![]()

[click each image to enlarge]

[click each image to enlarge]

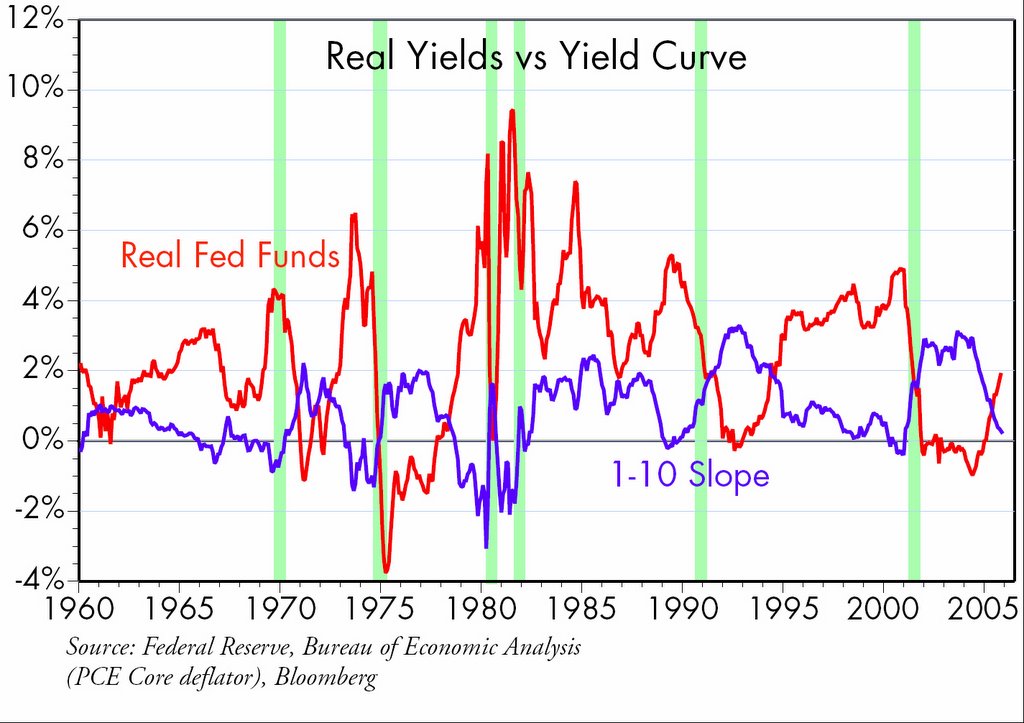

Outside of the aircraft industry, business "animal spirits" seem to have cooled. This is the first palpable sign since 2000 that the economy may be slowing down. This series is quite volatile, however, and dismissing the massive strength in the aircraft industry may exaggerate the degree to which the economy has actually slowed. But nevertheless it bears watching. I have thought that double-digit growth in this indicator was a key reason to be bullish on the economy over the past few years, so now, on the margin, the bullish case is harder to defend.

posted by David M Gordon | 6:21 AM

![]()

[click each photo to enlarge]

[click each photo to enlarge]

posted by David M Gordon | 6:03 AM

![]()

posted by David M Gordon | 8:19 AM

![]()

"Welcome to MarketGauge, the visually powerful trading and equity analysis tool that provides you with the best way to track industry group and sector rotation, generate stock ideas, and see what’s driving the market at every level."Comments?

posted by David M Gordon | 10:44 AM

![]()

JMP Securities raises their GOOG target to $575 from $400, as they believe the company is a clear winner in the AOL bake off. The firm's estimates suggest an even higher implied value for the AOL business than the $20 billion being reported in the media. They say that at $1.2 billion in cash and ad credits for a 5% stake, the deal would imply a value for AOL in the $25 bln range. From a strategic standpoint, they believe the deal gives GOOG multiple entres into the branded market, which is important for the company's long term growth outlook. Firm's confidence in Google's ability to meet or beat their estimates is higher than any other co in their coverage group, and they believe investors are likely to look farther out in the case of Google than most other Internet stocks.2) Something of an analysis, (shared via regular blog reader, Marty Safir)...

AOL, by the way continues to be the king maker in the Internet space, despite its troubles. I think many, scratch that, almost all have focused on the advertising aspect of this deal. In my mind, this is a deal which has larger strategic implications. The first - the instant messaging. The two companies explicitly state that they are going to interoperate their IM networks. For Google’s GTalk, this is a big boost, something it needed desperately in order to increase traction when compared to Microsoft and Yahoo. The IM alliance between Google-AOL is a good way to combat Microsoft-Yahoo IM combo.Wait, there is more...Continue reading, "Hey AOL, You Got Googled"

A few weeks ago, I promised to write a follow-up on my post about Google Base that detailed how the launch of Google Base might affect the Internet’s so-called “Walled Gardens” (content sites that charge users and/or suppliers for access to their databases). One month and a long cruise later, here it is...5) An interesting item from WIRED magazine...

It seems no one is safe: Google is doing Wi-Fi; Google is searching inside books; Google has a plan for ecommerce.Of course, Google has always wanted to be more than a search engine. Even in the early days, its ultimate goal was extravagant: to organize the world's information. High-minded as that sounds, Google's ever-expanding agenda has put it on a collision course with nearly every company in the information technology industry: Amazon.com, Comcast, eBay, Yahoo!, even Microsoft.

No more spam. No more "phishing" bank scams. News, pictures and short clips sent seamlessly to your phone ... or your fridge. Video conferencing that works first time, no hassles. Free, stereo-quality phone calls anywhere in the world. No, it's not a utopian ideal, it's the internet that some people will begin to experience in the next 12 months.Continue reading here...

Unknown to virtually everyone except IT engineers, the internet is being upgraded to a system called IPv6 (for Internet Protocol version 6)...

posted by David M Gordon | 5:24 AM

![]()

posted by David M Gordon | 9:49 AM

![]()

Ouch, what happened to IRIS today (Monday)? How does today's action affect your view/interest of that [former?] member of your winning list?Good lord, you do not think I am long each stock? It seems you did not read the post to its conclusion, so I quote again its real message... "Of course, there is this post's subject header. Qui vive means "alert, lookout" -- I am on the lookout always for changes. Negative change occurs in the market now, as former bullish patterns creak under the weight of their uptrends... These declines represent warning shots over the bow, or so goes my interpretation. Thus, I position my portfolio more defensively..."

Now that you've revealed that your trading price objective for GOOG was 600 a long time ago, would you please explain the method by which you arrived at that target whenever it was that you did. I look forward to studying your annotated charts whenever you post them.Long, long ago, when I was in elementary school, I learned the alphabet as did everyone else, including parts of speech (nouns, etc) and pronounciation, etc. Once learned, I suffered from the mistaken notion that we next would be taught how to read, to put together all the lessons into a unified whole. But no, we were taught only the rudiments; it then was up to us to place the lessons within a meaningful context.

Would people really complain if your target of 600 is off by a bit? I hope not. Actually, being off by a lot ~100 or more is still a bit. Most analysts will need to be raising their targets a few more times between now and 600 or so.You misunderstand the role of cause and effect. Unfortunately, you also misunderstand the intent of my comments, even though I stated them quite clearly. Or so I believe :-) Alas, misunderstandings such as yours are why I typically do not 'reveal' these price objectives. For the record, I figure ~75% of my trading objective has been reached, although not my investment objective, which is higher. GOOG has rallied to ~$450 from its IPO of $85 -- which itself is after my first recommendations of the investment. Try to lose this concept of predictions, correct and incorrect, and focus instead on your satisfaction. At what price are you satisfied?

I was hoping to get your thoughts on a company that I have followed for a long, long time. The company, named Inphonic/INPC...

[click to enlarge]

[click to enlarge]

Each bar highlighted in yellow is the stock's opportunity to cry, "Uncle" -- to reverse finally to up from down. Alas, it has failed in each instance, and does not appear this dynamic will change soon. Consider the cluster of bars in area #1, which manifests as horrible stochastics: the tendency for each day's bar to close on or near its lows. This down trend does grow long in the tooth, so I would monitor for that key reversal day. It has yet to arrive, however, so continuing new lows seems its near term destiny.

Speaking of key reversals days...

I was wondering if the up opening, peak pricing and lower close on GOOG was the signal you were discussing that might indicate an exit point is at hand. Or, was all that volatility just about the entry in the NASDAQ 100?Yes... and no. What you note is correct -- yesterday does qualify as a reversal day -- but is not the key reversal day I seek. GOOG

"I think the worm is about to turn on Google. The company's ascent has been too rapid, its successes too extravagant. As I wrote this sentence a few days ago, Google's stock price was $416, up more than 300 percent since the company went public a mere 16 months ago... Regular people look at that run-up and say: "Nice work, Google, you must be doing something right." Media people look at the same numbers and hear a little voice: Somebody's got to stop this."I find articles of this type to be silly; having missed making the bullish call, everybody and his or her uncle want now to make the bearish call. Yes, the share price will reverse, but we expect that. Please do not be surprised when it does finally occur.

posted by David M Gordon | 4:58 AM

![]()

I am long on LVLT and have been for sometime. I noticed today’s interesting trading activity. It looks to me like an institution dumped ~7-8 million shares late in the day. While this didn’t cause the stock to breach its 50 day it does show me someone is clearly headed for the exits. Would you view this as cause for concern or do you feel since the shares were absorbed by the market and the stock didn’t break the 50 day it’s a nothing to be alarmed about?Please recall that the NASDAQ 100 index makes changes effective with tomorrow’s opening: eleven stocks, including Level 3/LVLT, drop from the index in favor of eleven additions. So the large block or blocks you saw crossing likely was position squaring ahead of that event. As for the price declining to the 50 day simple moving average (sma), its relevance is dependent upon your time frame, risk tolerance, and objective -- none of which you betray, alas.

When goog went through $420, I gave up on AFL to buy more goog. It's probably a bad sign, but I wonder why I own anything but goog... I'm sure I'll get past it because diversification is a good thing.Comments of this type concern me. Diversification within reason (say, ~9 stocks) still has a place in the modern portfolio. Does the writer not realize the analogue between his perception of current opportunities and the market in 1999? Then, as well, investors crowded into the ever-fewer stocks that still performed (i.e., rose in price), thus powering them that much higher that much more quickly. The same occurs now for Google/GOOG. More players buy into a rising stock while other leaders crumble; this crowding likely will result in some exciting (read, fast) price appreciation near term. The following comment is from Tommy Dorsey at Dorsey Wright Analytics…

The main trend of GOOG remains positive and the stock has strong relative strength as you would suspect. The chart pattern has consolidated over the last couple of weeks to form a triangle pattern. That triangle pattern has now been completed with a double top breakout at 420. Typically, breakouts from bullish triangle patterns result in quick, explosive moves. With this breakout in GOOG, it provides an entry point for new positions with a stop or hedge point provided at 392, a spread double bottom, or 376, a violation of all near term support. The bullish price objective is, unbelievably, 608. We will see, but certainly the trend chart remains positive here.I have not previously uttered publicly this number but have held it in reserve for a l o n g time, this $600/share has been my trading objective for Google/GOOG -- possible to achieve by late-April 2006, perhaps sooner. It is also possible it fails to achieve that objective. At this moment, I watch the process itself; i.e., how the chart unfolds. I seek the setup for a key reversal day albeit at a higher price than the current $430.

posted by David M Gordon | 3:49 PM

![]()

I do not pretend to understand the dynamics of corporate strategy; perhaps there is something in this AOL deal that I fail to grasp or understand, perhaps even that the deal will revivify the crumbling corpse of AOL. That alone would make the deal worth doing, as it would bring with it a vibrant partner for Google, locked in at existing rates for the next 5 years, and possibly garner a return on its newly-acquired 5% holding. All that would be nice! Meanwhile, Google proceeds with its grand design, whatever that is. (To be revealed all in good time, Grasshopper. :-)And from Doug Casey at Casey Research comes this essay...

posted by David M Gordon | 9:17 AM

![]()

1157. (SA2005RF0096)

Wealth Tax. Tax Rates. Tax Credits. Initiative Constitutional Amendment and Statute.

Summary Date: 10/14/05 Circulation Deadline: 03/13/06 Signatures Required: 598,105

Proponent: Paul McCauley (818) 788-5919

Imposes one-time 45% tax on California residents and certain former California residents owning property worth more than $40 million on January 1, 2007. Amends Constitution to exempt this tax from 1% limit on ad valorem real property taxes. Imposes additional 12% tax on income for high-income taxpayers. Reduces corporate income tax rate by approximately 54%. Eliminates alternative minimum tax and certain tax credits, including those for head of household and dependants. Creates/increases tax credits, including those for teacher pay, public college tuition; property taxes and health insurance. Summary of estimate by Legislative Analyst and Director of Finance of fiscal impact on state and local governments: One-time increase in state revenues potentially up to $200 billion from imposition of a wealth tax. A portion of this revenue would be required to be allocated to schools with the remainder used for other state spending or tax rebates. Annual increased state taxes- primarily from increased personal income taxes- in the low tens of billions of dollars annually, offset by a commensurate amount of state tax reductions from rate reductions and new tax credits.

posted by David M Gordon | 8:30 AM

![]()

"Prudential raises their Teva Pharmaceuticals/TEVA tgt to $50 from $42, as they believe Copaxone and patent settlements help keep TEVA's earnings growth steady. Although they find it difficult to include generic launches in their model until they have a court win or other source of confidence, they feel the increased visibility these settlements provide should be reflected in a higher multiple on near-term earnings. Firm notes that Teva has already announced or executed agreements with GSK on Lamictal, WYE on Effexor/Effexor XR, BMY on Paraplatin and CEPH on Provigil. They believe Teva's portfolio of patent challenges is the largest of the generic companies (especially in combination with IVAX), and say additional settlement announcements are likely."And yes, I remain long the shares. Since the recommendation of TEVA, the share price has rallied to ~$45 from ~$35, a gain of ~35% in little more than two months. Not too shabby.

posted by David M Gordon | 6:26 AM

![]()

Dear David,Robert Koppel (link in sidebar) in today's mail. I jumped on the book and quickly turned to the table of contents to see which chapter was devoted to an interview with you. Ahhh, Chapert 9 "Seeing Is Believing". I have to say I never tire of how cool it is that I know you.

I just received the book Bulls, Bears, and Millionaires: War Stories of the Trading Life by

posted by David M Gordon | 5:22 AM

![]()

"Chart Patterns are the footprints of the smart money. Following those footprints can lead you to riches or disaster, depending on your experience tracking their signals. This page is the gateway to describing the shape of those footprints, what to look for, and how to trade their signals."Continue reading here... This site is so helpful and Thom's analysis so excellent (as always), that this link will be a permanent feature in the sidebar, under "Investing." By the by, Thom and I used to present (albeit not together, unfortunately) at Tim Slater's TAG seminars, which is where we first met, and how I came to know and respect the quality of his insights.)

posted by David M Gordon | 4:15 AM

![]()

Regarding JWN: I'm trying to learn about price action, notwithstanding all the other factors one should consider in an investment decision -- no analysis paralysis here but I wonder if you'd comment. The upside breakout hasn't occured yet, as I observe a consolidation rectangle happening since ~Aug 05. I see this in many time frames. To confirm the upside breakout we'd want to see a solid close above $38.50. Even then it'll likely retrace before going up to our first upside objective which would be ~$47 ($39 + 8pts, the depth of the rectangle, = $47). My question is this: what do you see? If the breakout is not confirmed yet, why do you buy? Are you seeing shorter time frame pattern(s) that confirm a good entry point, or are you looking at a longer time frame and see something else?

[click to enlarge]

[click to enlarge]

My earlier, private reply sucks...

You are so close to the trees you can see the gnarls in the bark — but not the forest. Shift periodicities. I think I will try again...

I have previously denoted my critical four items when parsing a chart: price, volume, pattern, and trend. I note in the chart of JWN, for example, that

1) The share price is very near its all time high (itself set ~3-4 weeks ago), that

2) The price:volume relationship remains fine across individual bars and the epochal pattern the writer delimits, that

3) The pattern offers every indication of being a base -- in fact, it is a short term (the past 3-4 weeks) base above an intermediate term base (the one notet) -- and not a top, and that

4) It remains within the boundaries of a long term up trend.

There comes that moment where you must trust the truth of the pattern, the trend -- and yourself. I return to this 'old' post, and ponder in particular these two insights that resonate for me, and arguably are applicable to this 'conversation'...

"Experts perceive patterns in their domain. Bill Chase and Herb Simon demonstrated this point with chess players. Rather than focusing on the position of individual pieces, expert chess players perceive clusters of pieces, or chunks. Estimates suggest that chess masters store roughly 50,000 chunks in long-term memory. Notably, this pattern recognition does not represent superior perception ability. When chess pieces are placed randomly on the board, experts remember the positions about as well as novices. The difference amounts to a database of chunks, amassed through deliberate practice, from which experts can draw." (Emphasis mine -- dmg)

and...

"Experts spend a lot of time solving problems qualitatively. When researchers present novices with a problem within a domain, the novices quickly go to relevant equations and solve for the unknown. In contrast, experts tend to create a mental representation of the problem, try to infer relations within the problem, and consider constraints that might reduce the search space. Domain knowledge and experience allow experts greater perspective on problem solving." (Emphasis mine -- dmg)

I have looked at so many charts and for so many years that I know how a pattern -- in truth,, many patterns -- fulfill themselves; i.e., complete the setup. For example, how many breakouts does the investor require ("The upside breakout hasn't occured yet") to know, to see, that the long term trend is up, as is the case for JWN? Breakouts occur from a pattern but within a trend; the continuum (more or less), as I term it.

Approximately 4-6 weeks ago, I recommended Dress Barn/DBRN, then at $25. It required the sudden lurch upwards to $35 before igniting the buying interest of most readers. Why should that be? I suspect it is because most investors draw a line of demarcation into the future from the moment they first notice or come upon an opportunity; their attention drawn to Dress Barn/DBRN at $25, they now see they gave up an easy and quick 40% gain. "Is it still okay to buy?", they wonder. To which I ask, "Why is it okay to buy at $35 and not $25...?"

Try this parallax view: select an opportunity that especially excites you, look at its pattern, step into the future, and look backwards in time from the moment in the future to today. Draw the line of demarcation from the future high rather than from the wholly arbitrary point that you stumbled upon the opportunity. You say you cannot do that, see the future? Then develop a repository of patterns and trends so that you know how they tend to fulfill and complete themselves. Cluster the information, the patterns, and the spatial contexts. From the same afore-mentioned research report ("Are you an expert?")...

• Successful investors put in plenty of deliberate practice. In investing, this generally means lots of time reading, often across diverse fields.

• Great investors conceptualize problems differently than other investors. As a group, these experts go beyond the near-term obvious issues, can identify relevant principles because of their experience, and see meaningful trends.

• Not pattern recognition but process recognition.

That is, the continuum. It is no different across the many opportunities I bring forth: JWN is no different than DBRN, or AAPL, CAKE, COH, DNA, GOOG, HOLX, MATR, NKE, NUVA, SBUX, SIRF, TEVA, TRID, WFMI... (I really, really must write a post updating my portfolio opportunities!) The patterns and setups might be dissimilar, but the trends remain the same -- up long term.

Have trust in youself that you always will do the right thing, make the hard decision. If you buy and the position instead declines, stop out. If you buy, but the position does not immediately rise or otherwise grieves you, then sell. But for god's sake, manage your positions, your cash, and your opportunities. You need not be always correct. And if you have proved to yourself congenitally unable to deploy such calculation in your financial dealings, then put into place a rules-based system to keep you from hurting your portfolio.

Traders and investors come in only two guises: intuitive and mechanical. (Scan ~¼ of the way down the page for the definitions.) Which are you?

"One cannot walk the Path until one becomes the Path"

-- Gautama Buddha

posted by David M Gordon | 3:19 AM

![]()

posted by David M Gordon | 2:39 AM

![]()

... That was a summary of just one chapter of ten in this book. The nine other [chapter]s similarly contain tradable observations about the human condition and how it works against even the best and brightest traders/investors. Although not yet through the book, I wanted to bring it to everyone's attention and to thank John publically for bringing it to mine. A good tip doesn't always have to involve a stock.

posted by David M Gordon | 2:33 AM

![]()

posted by David M Gordon | 8:03 AM

![]()

The expert-prediction game is not much different. When television pundits make predictions, the more ingenious their forecasts the greater their cachet. An arresting new prediction means that the expert has discovered a set of interlocking causes that no one else has spotted, and that could lead to an outcome that the conventional wisdom is ignoring. On shows like “The McLaughlin Group,” these experts never lose their reputations, or their jobs, because long shots are their business. More serious commentators differ from the pundits only in the degree of showmanship. These serious experts—the think tankers and area-studies professors—are not entirely out to entertain, but they are a little out to entertain, and both their status as experts and their appeal as performers require them to predict futures that are not obvious to the viewer. The producer of the show does not want you and me to sit there listening to an expert and thinking, I could have said that. The expert also suffers from knowing too much: the more facts an expert has, the more information is available to be enlisted in support of his or her pet theories, and the more chains of causation he or she can find beguiling. This helps explain why specialists fail to outguess non-specialists. The odds tend to be with the obvious.One important take away from reading this article is that, arguably, investors are different. We, too, must make predictions -- unlike all those other 'experts' Menand and Tetlock dissect and expose. However, we must assume ownership of our predictions, thanks to a concept known as mark to market. And if we do not assume ownership? Then our error-ridden predictions own us; aka, owning a portfolio of losers.

Tetlock’s experts were also no different from the rest of us when it came to learning from their mistakes. Most people tend to dismiss new information that doesn’t fit with what they already believe. Tetlock found that his experts used a double standard: they were much tougher in assessing the validity of information that undercut their theory than they were in crediting information that supported it. The same deficiency leads liberals to read only The Nation and conservatives to read only National Review. We are not natural falsificationists: we would rather find more reasons for believing what we already believe than look for reasons that we might be wrong. In the terms of Karl Popper’s famous example, to verify our intuition that all swans are white we look for lots more white swans, when what we should really be looking for is one black swan.

Also, people tend to see the future as indeterminate and the past as inevitable. If you look backward, the dots that lead up to Hitler or the fall of the Soviet Union or the attacks on September 11th all connect. If you look forward, it’s just a random scatter of dots, many potential chains of causation leading to many possible outcomes. We have no idea today how tomorrow’s invasion of a foreign land is going to go; after the invasion, we can actually persuade ourselves that we knew all along. The result seems inevitable, and therefore predictable. Tetlock found that, consistent with this asymmetry, experts routinely misremembered the degree of probability they had assigned to an event after it came to pass. They claimed to have predicted what happened with a higher degree of certainty than, according to the record, they really did. When this was pointed out to them, by Tetlock’s researchers, they sometimes became defensive.

posted by David M Gordon | 12:08 PM

![]()

posted by David M Gordon | 8:56 AM

![]()

posted by David M Gordon | 4:23 AM

![]()

posted by David M Gordon | 9:22 AM

![]()