Quickly, briefly...

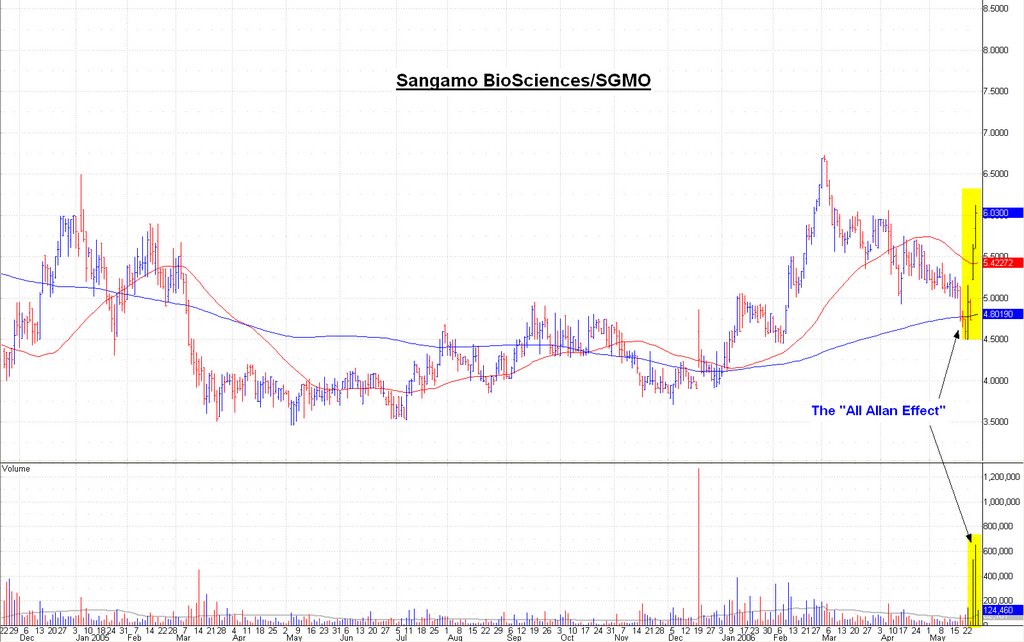

This sell-off in the markets not only re-asserts itself, but it worsens and thus likely deepens the location for the ultimate low. I retreated to cash weeks ago, and remain there. Trading positions prove ephemeral: AAPL, MRVL, and SNDK were each sold long ago; RACK likely soon. (It will most probably double-bottom, assuming the bullish resolution of this budding pattern.) Investment positions linger, as always.

New and interesting opportunities repeatedly crop up; however, the market is in buzz-saw mode -- it chops down everything within sight. Do not allow the market's many (bullish) feints to gull you; continue to trade carefully, diligently, and with close stops - as I warned ~3 weeks ago. Who knows how low, 'low' truly is...?

-- David M Gordon / The Deipnosophist

New and interesting opportunities repeatedly crop up; however, the market is in buzz-saw mode -- it chops down everything within sight. Do not allow the market's many (bullish) feints to gull you; continue to trade carefully, diligently, and with close stops - as I warned ~3 weeks ago. Who knows how low, 'low' truly is...?

-- David M Gordon / The Deipnosophist

posted by David M Gordon | 7:43 AM

![]()