My shopping list

I had mentioned that I continually update my shopping list, especially as the market makes large directional moves. My shopping list includes companies that I:

1) Invest in;

2) Trade around; or

3) Monitor closely, as a new opportunity.

If the specific opportunity fails to inspire interest as an investment, then I rarely, if ever, buy it as a trade. I seek an alignment of:

a) My needs;

b) The specific opportunity's placement within its continuum;

c) The near term direction of the market (an important distinction re time and the market that, if reminded, I will discuss in a future post)

When considering any opportunity, please recall the four critical criteria, as I deem them: price, volume, pattern, and trend.

THE LIST (with annotations)...

Abercrombie & Fitch/ANF -- see archives

American Eagle Outfitters/AEOS -- see archives

Apple/AAPL -- see archives

Bebe/BEBE -- breaking out as I type, albeit with insufficient volume

Cameco/CCJ -- leader in the uranium group, nice i/t base

Cheescake Factory/CAKE -- see archives

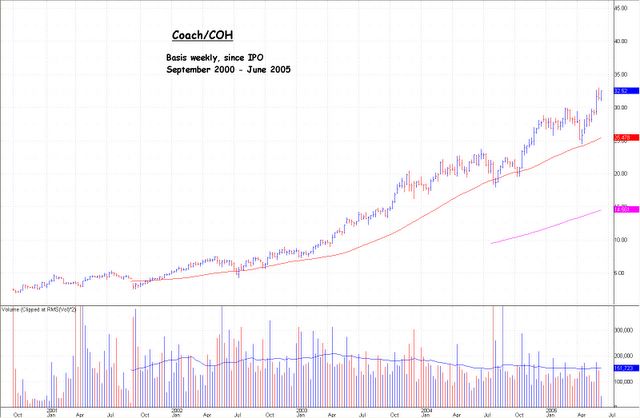

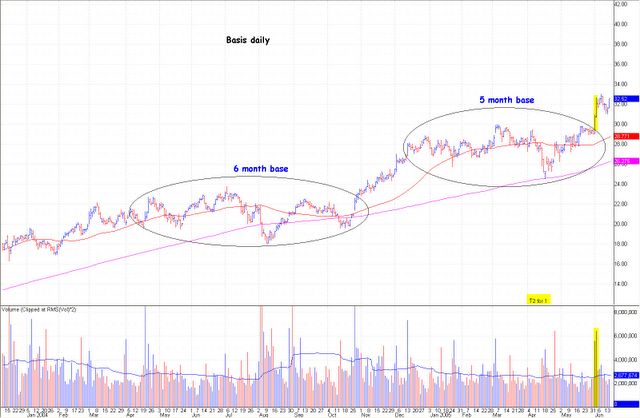

Coach/COH -- see archives

Domino's/DPZ -- potential short term base

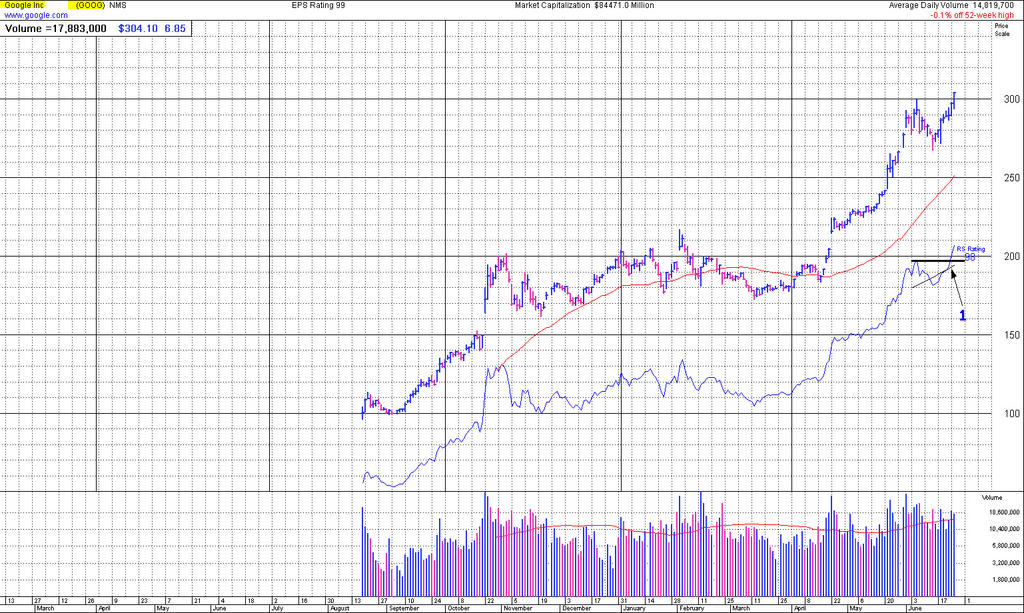

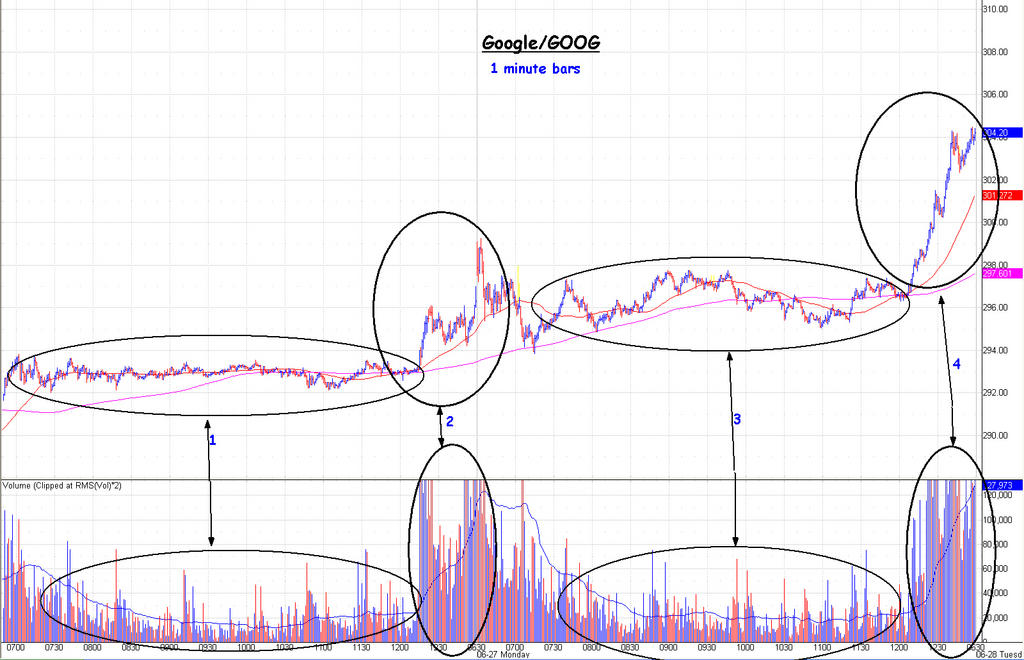

Google/GOOG -- did you think it would somehow not make this list?

Johnson & Johnson/JNJ -- very near its either-way inflection point; I believe that break will be up

Joseph Bank/JOSB -- see archives; potential short term base

Men's Wearhouse/MW -- see archives

PF Changs/PFCB -- see archives

Starbucks/SBUX -- Patience...

Station Casinos/STN -- potential intermediate term base

Syneron Medical/ELOS -- a reluctant inclusion

Timberland/TBL -- see archives

Urban Outfitters/URBN -- arguably the leader for stock performance among the specialty retailers

Whole Foods Markets/WFMI -- Price is immediately beneath its all time high; potential short term base.

(I might lose interest in any one of these opportunities -- or add new ones.)

And for those who like to hedge their longs with a few shorts, I would monitor the homebuilders, which might have put in their high trade, and now build a top -- or a base. Only the passage of time, and the subtle clues of course, will tell the tale.

Please share your questions, comments, and recommendations. (The last, with rationale included.)

1) Invest in;

2) Trade around; or

3) Monitor closely, as a new opportunity.

If the specific opportunity fails to inspire interest as an investment, then I rarely, if ever, buy it as a trade. I seek an alignment of:

a) My needs;

b) The specific opportunity's placement within its continuum;

c) The near term direction of the market (an important distinction re time and the market that, if reminded, I will discuss in a future post)

When considering any opportunity, please recall the four critical criteria, as I deem them: price, volume, pattern, and trend.

THE LIST (with annotations)...

Abercrombie & Fitch/ANF -- see archives

American Eagle Outfitters/AEOS -- see archives

Apple/AAPL -- see archives

Bebe/BEBE -- breaking out as I type, albeit with insufficient volume

Cameco/CCJ -- leader in the uranium group, nice i/t base

Cheescake Factory/CAKE -- see archives

Coach/COH -- see archives

Domino's/DPZ -- potential short term base

Google/GOOG -- did you think it would somehow not make this list?

Johnson & Johnson/JNJ -- very near its either-way inflection point; I believe that break will be up

Joseph Bank/JOSB -- see archives; potential short term base

Men's Wearhouse/MW -- see archives

PF Changs/PFCB -- see archives

Starbucks/SBUX -- Patience...

Station Casinos/STN -- potential intermediate term base

Syneron Medical/ELOS -- a reluctant inclusion

Timberland/TBL -- see archives

Urban Outfitters/URBN -- arguably the leader for stock performance among the specialty retailers

Whole Foods Markets/WFMI -- Price is immediately beneath its all time high; potential short term base.

(I might lose interest in any one of these opportunities -- or add new ones.)

And for those who like to hedge their longs with a few shorts, I would monitor the homebuilders, which might have put in their high trade, and now build a top -- or a base. Only the passage of time, and the subtle clues of course, will tell the tale.

Please share your questions, comments, and recommendations. (The last, with rationale included.)

posted by David M Gordon | 8:02 AM

![]()