Readers wonder, and ask often, whence come my investing ideas. No real surprises there -- from the usual suspects; either my familiarity with the company, its product or service, investment reports, or market action. My most reliable source, however, is from you.

"What do you think of this or that company or stock?" is the typical opening question. Included is an explanation of his or her interest. So I investigate. The first place is the historical chart: How compelling is this opportunity to consider it now? For example, I received during the weekend this message,

"I read your article on Under Armour - it was very interesting. I actually work with a company called Tefron/TFR that supplies Under Armour with a lot of their performance sportswear (as well as to Nike). I would be interested in hearing what you think about it."

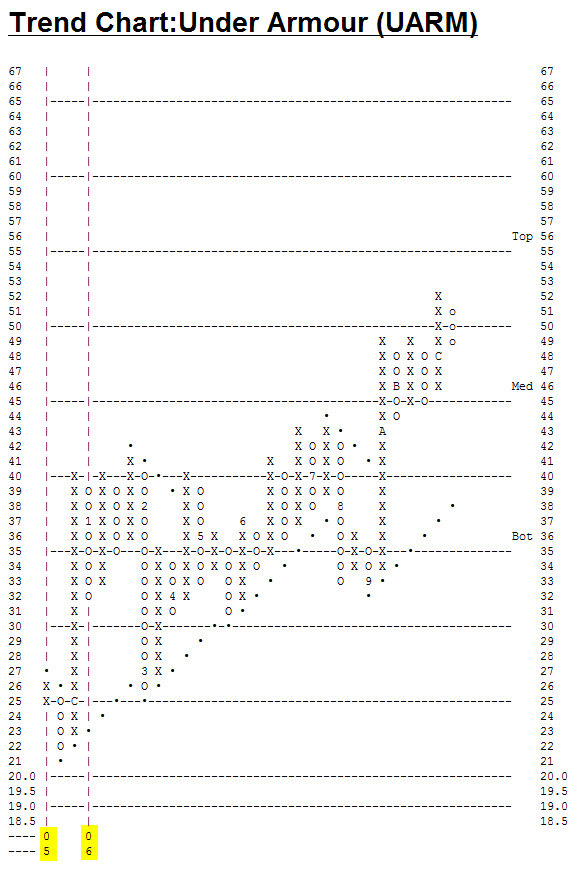

And so I look immediately at the historical chart of Tefron/TFR...  [click on image to enlarge]

[click on image to enlarge]

"Whoa!," I think. "Looks very interesting, enticing, even arguably immediately actionable!" Why is that? Because the rise in price from the bottom-clearing breakout above ~$6 (not drawn) during August 2005 until the reaction high trade of $13.73 during May 2006 was accompanied by an explosion of daily volume. I will confirm it next but can guess now: this company is in full turnaround mode. Turnaround, however, from what? How bad was the slump? How strong the recovery? Will that recovery continue?

These questions I will answer later. ("Answer" in the sense of best guess; none of us know the future.) So next I wonder, "Who wrote me?" Fortunately, the writer provided links, and I discern immediately the quality of his particulars and cv; he knows whereof he speaks.

Back to the charts. I focus next on the daily bars...

[click on image to enlarge]

[click on image to enlarge]"Whoa, redux!" Not only is Tefron, in a seeming turnaround, but its shares (TFR) scream, "Buy me. Now!" I see the powerful uptrend (already noted) with the comparatively massive and explosive volume; not solely leading, but also participatory. Investors want to own this stock despite rapidly climbing prices. The last 6+ months have traced out a very shallow decline, another designation of investors' demand for the shares. This will complete itself as an intermediate term base once through the line of declining tops (shown).

"Tefron manufactures intimate apparel, active-wear and swimwear sold throughout the world by such name-brand marketers as Victoria's Secret, Nike, Target, Warnaco/Calvin Klein, The Gap, Banana Republic, Mervyn's, Puma, Patagonia, Adidas, Reebok, and other American retailers and designer labels. Through the utilization of manufacturing technologies and techniques developed or refined by the Company, Tefron is able to mass-produce garments featuring designs tailored to its customers' individual specifications. For the nine months ended 30 September 2006, Tefron's revenues rose 10% to $138.1M. Net income from cont. ops. totaled $13.6M, up from $4.6M. Revenues reflect increased sales across all of the Company's product lines. Net income also reflects higher gross margins, lower financial expenses, improved operating margins due to increased production & lower labor costs."

The company stated only 4 months ago (Q2 earnings report), "Looking ahead, the company believes that it will achieve its target for 2006 of mid-teen percentage growth in revenues and profitability levels higher than those of 2005, at around the levels seen in the fourth quarter of 2005."

Hmmm, as a turnaround opportunity, this company and its shares become increasingly compelling. With this limited information, then, the game is afoot. How much more might I discover, how much more might I learn before this stock breaks out with renewed vigor to the upside? Because that is precisely what the stock has prepared itself to do. Go up. So the odds are that I will purchase soon an exploratory lot -- to establish an initial position in advance of the eventual lift-off from this base and while I do more investigatory (gumshoe) work. ("The soles of my shoes, Watson, wear out quickly!") Tefron, as you would imagine, is under-followed by Wall Street; another reason for my interest. Such lack of notice provides added goose to the upside as the analysts finally chime in (when they note the rising price and trend).

I do note, however, one caveat, one cavil: its average daily volume is so thin as to be comparatively illiquid. I want to participate but not initiate; i.e., I want to participate in the stock's rise, not initiate it. Too, I do not want to become the market -- both buyer and seller -- so my need for sufficient liquidity, offset by my portfolio's requirement for profits, has me return to the notion of money management: How many shares could I purchase that would make a notable impact on my portfolio's return on investment vs the seeming illiquidity. Aye, and there's the rub: seeming illiquidity because the average daily volume will increase as the share price trends higher.

So that is how I get from there to here, or whence and thence. More due diligence yet remains, and yet I know enough that I could purchase now the shares and make money. Again I think of the reader/writer... Thank you for bringing to my notice this opportunity. Write me again. Anytime. Soon, even.

-- David M Gordon / The Deipnosophist

Labels: Market analyses