masthead

posted by David M Gordon | 5:55 PM

![]()

Where the science of investing becomes an art of living

A private investor for 20+ years, I manage private portfolios and write about investing. You can read my market musings on three different sites: 1) The Deipnosophist, dedicated to teaching the market's processes and mechanics; 2) Investment Poetry, a subscription site dedicated to real time investment recommendations; and 3) Seeking Alpha, a combination of the other two sites with a mix of reprints from this site and all-original content. See you here, there, or the other site!

posted by David M Gordon | 12:14 PM

![]()

You can regale me with fine tales of how you were spared the ignominy of undiagnosed pain or spared death thanks in part to your health insurance. I would argue your story is the exception rather than the rule. Something is rotten in Denmark, as the article attests. HMOs, once regarded as savior of the entire industry, arguably are the largest contributor to the systemic problem. There is a failure in the system that lies somewhere between employer-sponsored health coverage, health insurance, doctors, and the patients. We each must give something to achieve balance.

I believe the system, as it is currently configured, is broken. What do you think...?

posted by David M Gordon | 4:37 PM

![]()

Once you have defined these facets of your trading plan, you are in an excellent position to have a strategy to control your emotions when trading. Make sure to review your plan on a regular basis to create effective trading habits.

posted by David M Gordon | 5:18 AM

![]()

Poetry is not to the tastes of everyone, nor even their sensibilities. This is due, in part, to the fact that proper methodologies for reading and enjoying poetry rarely are shared. Two tricks to increase your enjoyment:

This excellent poem (published in the Paris Review) is a fine opportunity to utilize these suggestions. Moreover, it is well-told, allusive, illusive, even elusive. I marvel at this author's talent.

The Alphabetizer Speaks

I have my reasons

have never known starvation nor plenitude

and unless the order of the world

changes, I won’t.

If the order of the world changes, I will

disappear, the way some vowels

elide into their word-bodies

or an individual blade recedes

into a field each season.

Will my daughter carry on this way?

I cannot yet tell her qualities—

if she prefers scale to chance, sequence to random.

And this may mean nothing.

I find chaos theory appealing, and eavesdrop on talk

of black holes, chasms, any abyss

that fetters sense. I relish

the desultory in many matters,

am slovenly, a slacker, a slave to caprice.

Except with the letters.

There is such thing as a calling

though I cannot speak for prophets or martyrs.

I have been summoned

by people of stature and the low-stationed,

comrade and debutante alike.

My eyes suffer, and my hands, my back.

I am my profession. It is no whim.

I do not want the world a certain way.

The world is that way, and I am a vehicle

on the road of nomenclature. I tend the road.

In my dream, all events coterminous—

no linear narrative, preceding or next.

The odd vignette, lone scene, an image

in isolation, no neighbors.

Then I awaken and pace

my thin balcony, calculating

how much of me waits above, how much

lives below, and I pose

the question of balance. My name

cues the turn home.

-- Patty Seyburn

posted by David M Gordon | 5:17 AM

![]()

posted by David M Gordon | 9:25 AM

![]()

In sum, while modest rebounding is possible today, further daily reaction lows are likely into the end of the week with the NASDAQ 100 breaking January levels.

I will discuss the intraday Futures patterns and the Dollar/Gold picture on this morning's conference call at 8:45 EST.

posted by David M Gordon | 5:21 AM

![]()

posted by David M Gordon | 7:31 AM

![]()

posted by David M Gordon | 10:10 AM

![]()

posted by David M Gordon | 9:45 AM

![]()

... makes this article perfect fodder for inclusion to this blog.

posted by David M Gordon | 10:24 AM

![]()

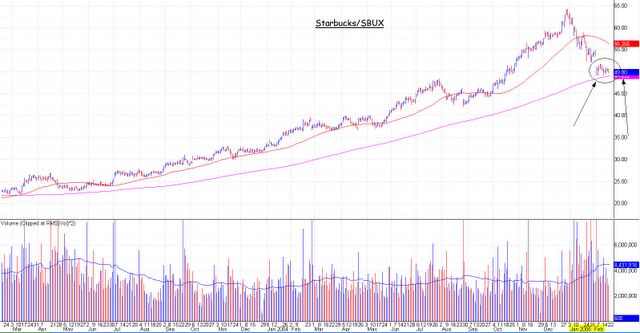

Should the former occur, then the shares soon will rise because the ma itself is rising! And should the latter instead occur, then at some moment soon thereafter, the shares will rally back toward the 200-day sma to prove that what once was support now is resistance.

So a purchase at this level can be either profitable or breakeven. Acknowledging the 7 weeks of near straight line decline adds fodder to the argument (at least) for a counter-trend move back toward the 50-day sma.

Whichever event occurs next, the subsequent rally -- toward the 50-day or a break beneath and rally back toward the 200-day -- will offer a significant tell for SBUX in the coming weeks and months. That is, was $64+ a final high (and thus making a statement re future growth) or merely another intermediate term high trade in its continuing long term uptrend?

Investing requires discipline, not hope or lazy thinking. One method to assure making profits consistently is to manage risk. I like my odds at this level: risk = ~$1 and reward = ~$6. Moreover, we should know soon which direction SBUX breaks. In the face of such uncertainty -- and because I believe the long term growth will continue -- I am a buyer of SBUX shares today @ $49.80 or better. I will not pay pay up, and buy at $52, $51, or even $50/share in the ignoble quest for ratification of the pattern.

At this moment, SBUX shares might represent continued risk to decline further, but having patiently bided my time until this moment, it is in truth a calculated risk, arrived at with dispassion.

posted by David M Gordon | 5:41 AM

![]()

posted by David M Gordon | 7:23 PM

![]()

posted by David M Gordon | 7:14 PM

![]()

posted by David M Gordon | 6:29 PM

![]()

posted by David M Gordon | 7:21 AM

![]()

Cheesecake Factory/CAKE ($34.10):

The main trend of CAKE is positive and the stock has three out of five technical attributes positive. The chart patterns show several classic patterns like:

In addition to completing this bullish catapult, the weekly momentum has flipped positive. Okay to buy CAKE here with a stop/hedge point at 29, a double bottom.

Comments above and chart (c) Dorsey Wright ~~~~~~~~~~~~~~~~~~~~~~~~~~~

Please visit a Cheesecake Factory near you (better, eat there), and note its attractiveness, its ambience, its food -- every item is yummy! -- and the long lines to get a table. This wait is true no matter which Cheesecake Factory you visit. I have had to wait at

So here's the thing: what are the reasons you invest? Could these attributes (not solely the wait, but the other items noted above) be an indicator of sorts...?

posted by David M Gordon | 4:51 AM

![]()

Many critics consider this art (by Sir Edwin Landseer) as maudlin, mawkish, even lachrymose.

[click to enlarge]

And yet I consider it to be, at minimum, a masterpiece of indirect storytelling, in addition to composition, technique, light, shading, and etc. Consider how much is said but with so little:

● Someone has died (by unknown circumstances),

● It seems noone has come to the funeral (the coffin is not yet in the ground) thus confirming a lonely existence, and

● The shepherd's dog -- likely the sole company for each other -- now misses his master. (One very subtle trick Landseer uses well is to curl inwards the dog's front right paw. Not to wax anthropomorphic, but this 'action' is among those that endears dogs to us humans. If instead Landseer had painted the dog sitting four-squarely, the dog's -- and our -- sense of loss would be missing. Techniques such as this one illustrate how art becomes Art, even a masterpiece.)

So from this scene of a funeral, our thoughts wander all the way from, "What happened?" to "What of the dog now?"

Anyone want to take this dog home...?

posted by David M Gordon | 2:54 AM

![]()

posted by David M Gordon | 6:45 PM

![]()

Labels: Book review, Humanities

posted by David M Gordon | 7:34 AM

![]()

posted by David M Gordon | 6:11 AM

![]()

posted by David M Gordon | 5:24 PM

![]()

posted by David M Gordon | 5:01 AM

![]()

BTW, this essay is not about Wal-Mart (although my quotes selections might lead you to think that), nor is it about the ostensible purpose behind the Procter&Gamble-Gillette merger, which is its purported topic. No, this essay is about something other.

Which is as it should be in order to be considered as among the few journalists of especial note: edifying content, depth of insights, and all told entertainingly well.

posted by David M Gordon | 9:16 AM

![]()

posted by David M Gordon | 4:35 AM

![]()

posted by David M Gordon | 6:03 PM

![]()

posted by David M Gordon | 2:14 PM

![]()

posted by David M Gordon | 9:57 AM

![]()

posted by David M Gordon | 4:17 AM

![]()

posted by David M Gordon | 2:23 AM

![]()

posted by David M Gordon | 6:11 PM

![]()

posted by David M Gordon | 10:00 AM

![]()

posted by David M Gordon | 1:16 AM

![]()

posted by David M Gordon | 1:08 AM

![]()

posted by David M Gordon | 1:04 AM

![]()

posted by David M Gordon | 1:02 AM

![]()

posted by David M Gordon | 1:01 AM

![]()

{kind=link}